{kind=link}

For years, myself, and plenty of others have thought that rates of interest had been the predictor of housing costs. Quick ahead to submit COVID the place rates of interest have doubled and but housing costs stay excessive and are nonetheless trending increased in lots of markets. What different metric ought to we watch to see the place housing costs are heading? Trace, take a look at the chart above.

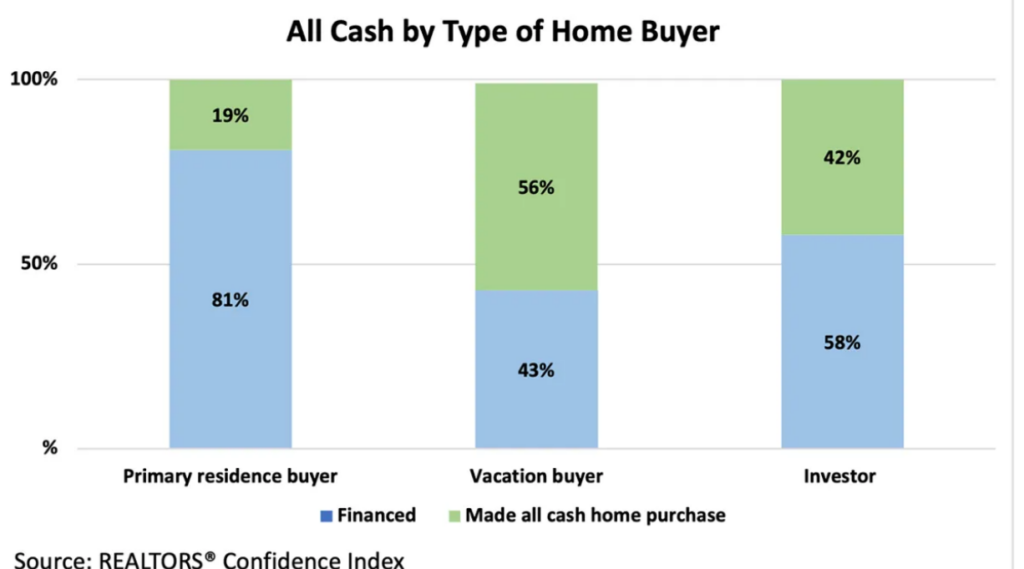

Trying on the information, there may be an fascinating development occurring because of the wealth impact of the inventory market. The proportion of all money patrons elevated particularly for trip/second houses during the last 5 years. Why are money patrons rising and what does this imply for actual property costs? Moreover, how is the wealth impact impacting costs? What does the inventory market imply for housing costs this 12 months and over the subsequent decade?

All Money patrons improve

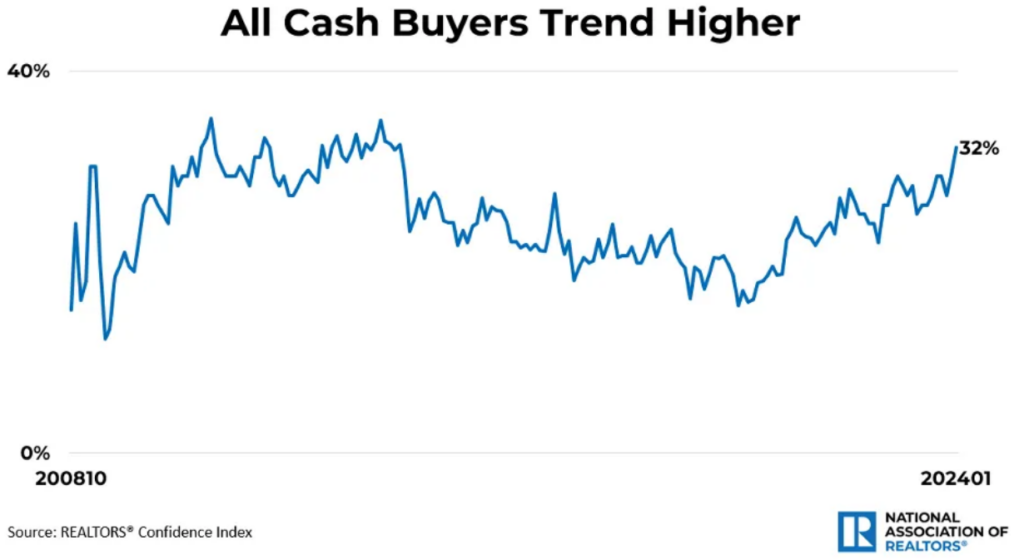

Whereas mortgage rates of interest have greater than doubled lately, the share of all money patrons is rising. all money dwelling patrons have trended up considerably in current months. Since October 2022, all money dwelling patrons who didn’t finance their current dwelling buy have been greater than one-quarter of the true property market. In January 2024, all money patrons now stand at 32% of dwelling gross sales. The final time the share of all money patrons was this excessive was June 2014. From the chart it’s straightforward to see why many trip markets have been supercharged as over half of the patrons are money. This additionally explains why rates of interest have had much less of an affect with so many properties being purchased with money.

Excessive correlation between inventory market and actual property costs

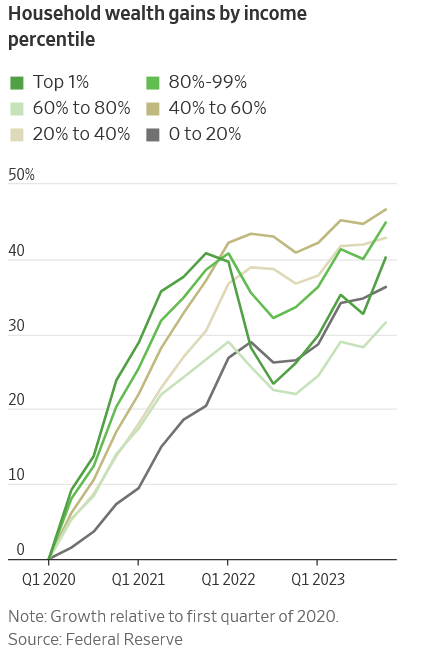

Together with money patrons, the inventory market has been on a tear till not too long ago. Prior to now, rates of interest had been the first driver of actual property costs, as charges moved considerably increased, property values dropped. This has not occurred on this cycle as a result of as charges moved considerably increased so did virtually each different asset from shares to bitcoin to many commodities. This has created a considerable wealth impact for many Individuals as proven within the chart under. The quantity of wealth created on this cycle is astounding.

This wealth has allowed extra folks to purchase properties all money and/or take up increased costs. Because the inventory market stays excessive so have housing costs and the correlation between the 2 has solely elevated through the submit pandemic cycle.

Excessive actual property costs making a constructive reinforcement loop

Together with the inventory market, the excessive worth of homes themselves is now preserving costs excessive making a loop impact. If you’ll promote your own home, you may get considerably greater than 5 years in the past, it will allow many patrons to purchase their subsequent home in money particularly in the event that they transfer to a decrease price space. This in flip is driving up costs in cheaper markets as there may be extra demand from different areas.

Rates of interest increased for longer than market thinks

Housing is the primary driver of inflation comprising over a 3rd of the buyer worth index. As housing costs keep increased together with rents, will probably be tough to see a serious reset in inflation. The market is at the moment pricing in a number of cuts to charges later this 12 months. I don’t foresee an enormous motion in charges based mostly on the wealth impact highlighted above.

Costs will proceed to remain excessive till inventory market reset

Costs of homes will proceed close to their peak till there’s a inventory market reset and folks “really feel” much less rich. At the moment rates of interest right now are possible not excessive sufficient for this to happen which can hold the federal reserve on a path for increased for longer till there’s a main reset in asset costs. With out a reset within the inventory market and in flip housing the economic system can be caught the place it’s right now for a bit longer. The million greenback query is that if this current hiccup within the inventory market is a large enough reset to radically alter actual property’s trajectory heading into the spring season?

Large modifications in long-term forecasts for the inventory market

The headline says all of it “ Decade of huge S&P 500 positive factors is over”. The predictions for the inventory market are fairly grim:

” US shares are unlikely to maintain their above-average efficiency of the previous decade as buyers flip to different property together with bonds for higher returns, Goldman Sachs Group Inc. strategists stated.

The S&P 500 Index is predicted to submit an annualized nominal complete return of simply 3% over the subsequent 10 years, in accordance with an evaluation by strategists together with David Kostin. That compares with 13% within the final decade, and a long-term common of 11%.

Additionally they see a roughly 72% probability that the benchmark index will path Treasury bonds, and a 33% probability they’ll lag inflation via 2034.”

Basically actual property rode the asset appreciation wave of the inventory market up and is now married to the brand new actuality of considerably decrease returns. Based mostly on the predictions of Goldman Sachs this may correlate to an analogous state of affairs for actual property with returns averaging round 3% over the subsequent 10 years, it is a enormous drop from the 20%+ we noticed some years through the Covid increase.

Extra correlation means larger draw back threat

Though the wealth impact has created enormous positives for the housing market with secure to rising costs in face of upper rates of interest, the get together can’t final without end. Sadly we have now already seen the upside during the last 10 years or so.

The draw back threat is more likely. With the large run ups in wealth and the traditionally robust inventory market there’s a a lot increased correlation between housing and the inventory market. As one goes down so will the opposite. As we have now seen all through the years in economics, excessive correlations are nice when markets are rising however when the winds change and there’s a reset, the draw back threat is amplified.

At the moment with asset values wobbling we haven’t seen a lot change in actual property values but, however the information says that change is underfoot. The elevated volatility within the inventory market needs to be a wakeup name because the inventory market doesn’t go up into perpetuity. Moreover, values are extraordinarily lofty based mostly on any historic metric which additional improve the danger of a fair bigger correction.

A reset within the inventory market will in the end result in a a lot larger reset in actual property values than prior to now because of the increased correlation. The million greenback query is when will this happen and the way a lot will housing costs drop. My intestine says that later this 12 months or early subsequent 12 months, the reset will happen because the the whole lot rally in shares and different property peters out, however the true story is that the last decade of big actual property positive factors is probably going over identical to we are going to see within the inventory market which implies housing costs are principally going to remain at greatest case even with inflation (principally 2-3% a 12 months for the subsequent 10 years) for the subsequent decade or worst case have a reset and underperform inflation.

On a facet notice, keep in mind that actual property is market particular so sure cities will carry out higher than others because of demographic shifts, worth factors, and so forth… that may alter particular person actual property markets. Dearer markets, like Denver can be hit tougher than different markets as the typical worth is over 600k that means most of the potential patrons at this worth level possible have substantial publicity to the inventory market.

Whatever the market, the times of all property rising in concord is beginning to reverse as we will see within the inventory market. There can be alternatives however will probably be significantly harder than the previous 10 years the place all you needed to do was purchase a property with 4 partitions and you would generate income.

Further Studying/Sources:

We’re a Personal/ Laborious Cash Lender funding in money!

Glen Weinberg personally writes these weekly actual property blogs based mostly on his actual property expertise as a lender and property proprietor. I’m not an armchair reporter/author. We’re an precise non-public lender, lending our personal cash. We service our personal loans and personal business and residential actual property all through the nation.

My day job is and continues to be non-public actual property lending/ arduous cash lending which permits me to have a novel perspective in the marketplace. I don’t settle for any paid sponsorships or advertisements on my weblog to make sure correct info. I’ve been scripting this for nearly 20 years and have over 30k subscribers. Please like and share my blogs on linkedin, twitter, fb, and different social media and ahead to your mates . I might enormously admire it.

Fairview is a arduous cash lender specializing in non-public cash loans / non-bank actual property loans in Georgia, Colorado, and Florida. We’re acknowledged within the trade because the chief in arduous cash lending/ Personal Lending with no upfront charges or every other video games. We fund our personal loans and supply trustworthy solutions rapidly. Be taught extra about Laborious Cash Lending via our free Laborious Cash Information. To get began on a mortgage all we want is our easy one web page software (no upfront charges or different video games).

Written by Glen Weinberg, COO/ VP Fairview Business Lending. Glen has been revealed as an knowledgeable in arduous cash lending, actual property valuation, financing, and numerous different actual property subjects in Bloomberg, Businessweek ,the Colorado Actual Property Journal, Nationwide Affiliation of Realtors Journal, The Actual Deal actual property information, the CO Biz Journal, The Denver Put up, The Scotsman mortgage dealer information, Mortgage Skilled America and numerous different nationwide publications.

Tags: Laborious Cash Lender, Personal lender, Denver arduous cash, Georgia arduous cash, Colorado arduous cash, Atlanta arduous cash, Florida arduous cash, Colorado non-public lender, Georgia non-public lender, Personal actual property loans, Laborious cash loans, Personal actual property mortgage, Laborious cash mortgage lender, residential arduous cash loans, business arduous cash loans, non-public mortgage lender, non-public actual property lender