{kind=link}

In nearly each actual property commercial I obtain, there’s a widespread theme that potential consumers shouldn’t deal with the speed as they’ll be capable of refinance comparatively quickly at a a lot decrease price. How true is that this concept? (trace anybody who purchased into this concept is in line for a shotgun marriage ceremony) Are charges going to drop rapidly like in previous cycles? Why are charges primed to remain larger for longer and what does this imply for residential and industrial actual property.

30 yr bond predicts long run inflation

Though the 30 yr bond just isn’t the ten yr treasury that’s principally the “peg” for mortgage charges, it does present the long run market expectations for treasuries and in flip mortgage charges. If we take a look at the chart above the most recent predictions from Wells Fargo present that 30 yr charges will stay about the place they’re at this time give or take ½%.

I’d agree with Properly’s predictions as authorities spending is off the charts each within the US and all through the world which is able to finally result in considerably extra treasuries on the market and finally larger charges (keep in mind treasury costs and charges work in inverse).

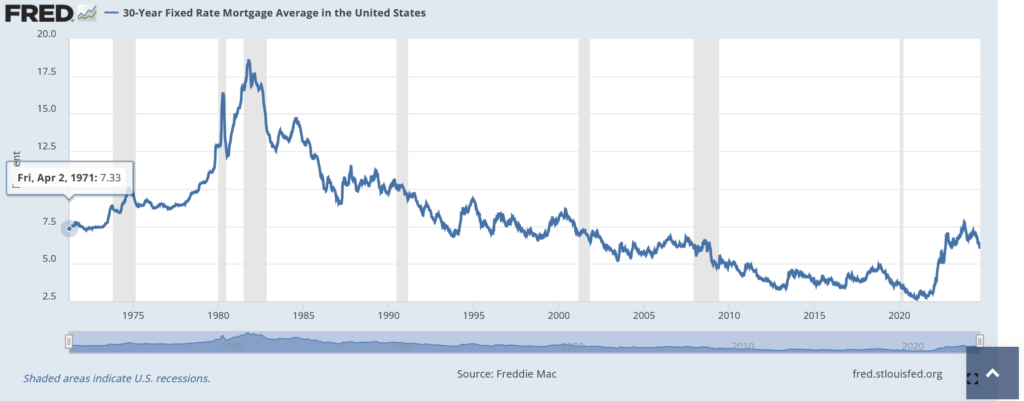

Mortgage price predictions are unsuitable, they are going to be a lot larger for longer

Should you take a look at any mainstream actual property publication, rates of interest are predicted to fall properly under the place they’re at this time. Sadly, I feel these predictions are useless unsuitable. To find out the place mortgage charges shall be in 2026 if I lined up the 30 yr historic chart above together with the historic mortgage chart under, it implies that charges shall be similar to the place they have been in 2008 which might put mortgage charges via 2026 within the 6.5 to 7.5% vary which is about the place they’re now.

Even wanting past 2026 price doubtless will keep properly above the extremely low charges from 2009 to 2019 as authorities spending ramps up which is able to preserve charges significantly larger than the final 10 years.

What do 6.5% and above charges imply for residential and industrial actual property?

With charges staying larger for longer there shall be big impacts on actual property costs:

Residential: Larger charges finally will result in declining costs particularly in larger priced markets as much less folks can afford to buy costly homes. Assuming a 500k mortgage at a 4% price precovid the funds can be 2,387/month, now quick ahead and that very same mortgage can be 3160/month. That is an additional 9300/yr in mortgage funds. This big bounce in funds doesn’t work for many potential consumers which is able to finally result in costs falling as a way to enhance affordability. The million greenback query is how a lot? I feel most markets will reset to the tune of 10-15% with some even larger.

Business: Now we have not even come near seeing the underside within the industrial market. As charges stay larger cap charges may also must rise which is able to finally result in a a lot deeper reset in industrial property values. Billions in mortgages are going to reset over the subsequent few years and for now lenders have kicked the can down the street however as charges stay larger for longer finally the market should face the music of a lot decrease property values. For instance, I’ve seen workplace buildings buying and selling at 20-30% off their values from only a few years in the past. Additionally, you will see an additional reset in multifamily and retail as cap charges are approach too low with treasuries staying larger for longer.

Marry the home/ date the speed

The belief on this evaluation to Marry the home and date the speed which means that the home is a long run dedication, however it is possible for you to to rapidly refinance right into a a lot decrease price just isn’t holding true.

Based mostly on elementary adjustments in productiveness, compensation, and so forth… charges are prone to keep significantly larger than anticipated and certain won’t ever return to the two.5-4% vary for 5-10 years. Moreover, authorities spending remains to be off the charts which is able to put additional stress on bond costs and in flip enhance yields. Because of this, we’ll see rates of interest within the 6-8% vary within the subsequent 7-10 years or so. I do know this can be a big vary, however the development is what’s vital in that charges shall be considerably larger than in the event that they have been pre-pandemic.

Shotgun marriage ceremony forward for folks relationship the speed

Sadly, the advertising mantra to marry the home and date the speed is proving to be false. Primarily anybody banking on a fast drop in charges is mistaken and simply received married to the home and price by way of a shotgun marriage ceremony. On account of a lot larger labor compensation by Airways, UPS, and numerous others together with loopy authorities spending inflation will stay stubbornly above the federal reserve’s 2% goal.

With inflation persevering with to be stickier than the market anticipates treasuries and in flip mortgage charges will stay significantly larger for longer. I anticipate mortgage charges to remain north of 6.5% for the subsequent 5 years (or probably eternally as that is about the long run mortgage price common) which is able to give debtors restricted potential to refinance to avoid wasting substantial cash.

Moreover I don’t foresee charges dropping to pandemic lows for fairly some time if ever as this was a as soon as in a lifetime occasion that prompted the federal reserve to purchase mortgages on the similar time they pushed down long run charges.

On account of excessive charges, search for actual property volumes to remain low for a while as there may be little incentive for folks to maneuver which have a low price. The actual query is consumers that find yourself with a shotgun marriage to a a lot larger rate of interest for for much longer than they anticipated.

Mortgage charges keep larger for longer

The market is useless unsuitable on the idea that rates of interest will quickly fall anytime quickly. We’re already seeing this play out at this time with the fed’s ½% lower mortgage charges finally elevated nearly ½% versus reducing. Sadly, bigger authorities spending and the push for a delicate touchdown will preserve long run charges like mortgages a lot larger for for much longer than is being priced in.

Because the market hasn’t come to phrases with larger for longer, the market is grossly underestimating the impacts to residential and industrial actual property. With mortgage charges above 6% via 2026, each residential and industrial actual property is primed for a considerable correction as the present costs aren’t sustainable in a better price surroundings. For instance, why would somebody purchase a industrial property on a 4-5% cap once they can purchase a authorities bond with the identical return with zero danger. Sadly, they might not, which suggests costs should alter downward.

Sadly predicting when the reset will happen is difficult as macro components like a warfare, surge in oil costs, tariffs, inventory market meltdown, and so forth… can occur quickly and drastically alter any predictions. With that stated, my finest guess is the second half of 2025 is after we begin seeing actuality set in because the market involves grips that low long run charges aren’t going to bail out the true property market as charges keep larger for longer.

Further Studying/Assets

- https://fred.stlouisfed.org/sequence/MORTGAGE30US

- https://econforecasting.com/forecast/t30y

- https://www.fairviewlending.com/fed-cuts-rates-why-are-mortgage-rates-rising/

- https://www.fairviewlending.com/commercial-real-estate-what-is-causing-the-decline/

- https://transportgeography.org/contents/chapter5/air-transport/airline-operating-costs/

- https://apnews.com/article/united-airlines-pilots-pay-raise-d1cf2dcd38d0d267bf8cfd8c652c6750

- https://www.ustravel.org/analysis/monthly-travel-data-report

- https://www.wsj.com/articles/ups-teamsters-reach-agreement-on-new-contract-a134c910?mod=article_inline

We’re a Personal/ Arduous Cash Lender funding in money!

Should you have been forwarded this message, please subscribe to our publication

Glen Weinberg personally writes these weekly actual property blogs based mostly on his actual property expertise as a lender and property proprietor. I’m not an armchair reporter/author. We’re an precise personal lender, lending our personal cash. We service our personal loans and personal industrial and residential actual property all through the nation.

My day job is and continues to be personal actual property lending/ exhausting cash lending which allows me to have a novel perspective in the marketplace. I don’t settle for any paid sponsorships or adverts on my weblog to make sure correct data. I’ve been penning this for nearly 20 years and have over 30k subscribers. Please like and share my blogs on linkedin, twitter, fb, and different social media and ahead to your pals . I’d significantly recognize it.

Fairview is a exhausting cash lender specializing in personal cash loans / non-bank actual property loans in Georgia, Colorado, and Florida. We’re acknowledged within the trade because the chief in exhausting cash lending/ Personal Lending with no upfront charges or another video games. We fund our personal loans and supply trustworthy solutions rapidly. Study extra about Arduous Cash Lending via our free Arduous Cash Information. To get began on a mortgage all we’d like is our easy one web page utility (no upfront charges or different video games).

Written by Glen Weinberg, COO/ VP Fairview Business Lending. Glen has been printed as an skilled in exhausting cash lending, actual property valuation, financing, and varied different actual property subjects in Bloomberg, Businessweek ,the Colorado Actual Property Journal, Nationwide Affiliation of Realtors Journal, The Actual Deal actual property information, the CO Biz Journal, The Denver Put up, The Scotsman mortgage dealer information, Mortgage Skilled America and varied different nationwide publications.

Tags: Arduous Cash Lender, Personal lender, Denver exhausting cash, Georgia exhausting cash, Colorado exhausting cash, Atlanta exhausting cash, Florida exhausting cash, Colorado personal lender, Georgia personal lender, Personal actual property loans, Arduous cash loans, Personal actual property mortgage, Arduous cash mortgage lender, residential exhausting cash loans, industrial exhausting cash loans, personal mortgage lender, personal actual property lender