{kind=link}

In my final weblog publish, Largest mortgage patrons required to make use of cryptocurrencies. There was a transparent consensus of whether or not the federal government ought to or shouldn’t be embracing crypto. However the responses had been thought frightening and the outcomes weren’t as clear minimize as I had thought. Thanks to everybody to your responses and perception, it’s invaluable. Beneath I’ll share the main points.

About my electronic mail checklist

My electronic mail checklist is massive and all natural that features realtors, appraisers, property house owners, assessors, varied actual property media, and so on… It’s a numerous group from a realtor in Atlanta specializing in 400k homes to a realtor in Telluride that simply bought a 50 million greenback residence. The viewpoints are numerous primarily based on geography, specialization inside actual property (title firm versus business property proprietor), and so on… This permits a novel cross perspective on actual property developments.

What was the query within the survey?

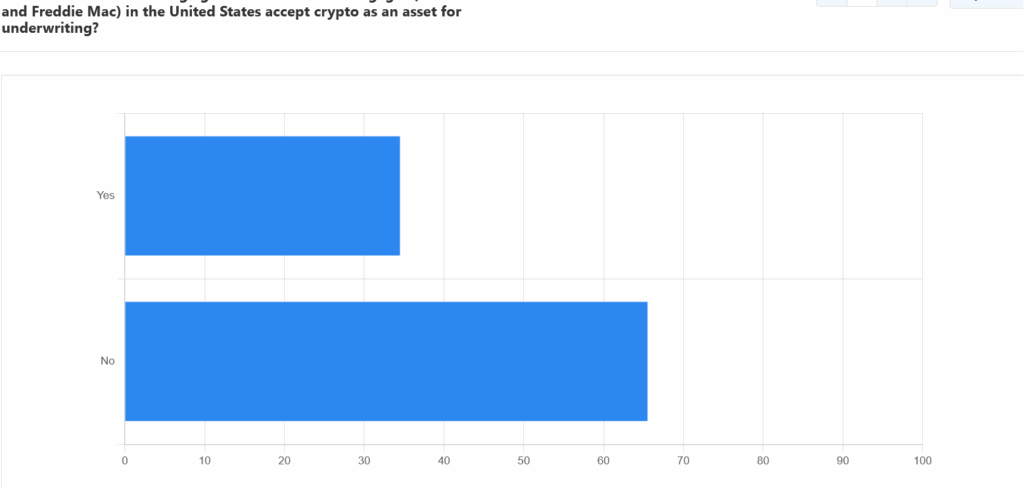

Ought to the federal housing businesses that insure mortgages (Fannie Mae and Freddie Mac) in the US settle for crypto as an asset for underwriting?

Sure

No

Please clarify why the US authorities ought to both settle for or decline crypto belongings for the aim of underwriting.

What had been the outcomes from the crypto survey?

I used to be amazed at how resounding the responses had been.

- 65% stated the federal government mustn’t settle for crypto as an asset for a mortgage

- 35% stated that the federal government ought to settle for crypto.

I additionally requested what the explanations behind the alternatives had been and listed here are the highest 5 responses

- If one can use shares why not crypto at this level?

- The worldwide economic system is witnessing the convergence of three enormous applied sciences, robotics, AI, and blockchain/cryto. Our world is transferring right into a extra digital world. With the signing of the Genius Act, and the US authorities positioning the US to be the chief of cryptocurrencies, particularly with the adoption of stablecoins, this administrative shift indicators the adoption of digital belongings.

- DECLINE as a result of it’s such an unstable and unstable “forex” secured by nothing apart from wishful pondering, it has no intrinsic worth. If a borrower can’t convert their crypto forex into sufficient precise cash for a partial or full cost for actual property, the general public shouldn’t be on the hook to transform an unstable asset into actual property. An unsecured promissory notice has a extra secure worth.

- Crypto is extraordinarily unstable, worth clear, and liquid. This makes it just like sure public market equities—like micro-caps. Looks like the underwriting tips for equities ought to apply to crypto. I’m no crypto fan, however I had been a lender, I’d desire to see crypto over belongings like artwork or small firm fairness. —nice publication subjects, thanks!

- Taxpayers might be on the hook for enormous losses as there isn’t a method to precisely worth crypto right this moment with the massive volatility it it too speculative

Abstract

Thanks everybody to your participation and insights in my survey. The overwhelming sentiment (65%) feels that crypto shouldn’t be used for mortgage underwriting, however 35% assume simply the other with some legitimate responses evaluating crypto to small cap shares which is probably going true from a threat perspective. Keep tuned for future surveys and outcomes.

Further Studying/Sources:

https://www.fairviewlending.com/largest-mortgage-buyers-required-to-use-cryptocurrencies/

https://www.fairviewlending.com/will-real-estate-fall-to-2020-values/

We’re a Personal/ Onerous Cash Lender funding in money!

Glen Weinberg personally writes these weekly actual property blogs primarily based on his actual property expertise as a lender and property proprietor. I’m not an armchair reporter/author. We’re an precise non-public lender, lending our personal cash. We service our personal loans and personal business and residential actual property all through the nation.

My day job is and continues to be non-public actual property lending/ arduous cash lending which allows me to have a novel perspective available on the market. I don’t settle for any paid sponsorships or adverts on my weblog to make sure correct info. I’ve been penning this for nearly 20 years and have over 30k subscribers. Please like and share my blogs on linkedin, twitter, fb, and different social media and ahead to your folks . I might significantly recognize it.

Fairview is a arduous cash lender specializing in non-public cash loans / non-bank actual property loans in Georgia, Colorado, and Florida. We’re acknowledged within the trade because the chief in arduous cash lending/ Personal Lending with no upfront charges or some other video games. We fund our personal loans and supply sincere solutions shortly. Study extra about Onerous Cash Lending by our free Onerous Cash Information. To get began on a mortgage all we want is our easy one web page utility (no upfront charges or different video games).

Written by Glen Weinberg, COO/ VP Fairview Industrial Lending. Glen has been revealed as an professional in arduous cash lending, actual property valuation, financing, and varied different actual property subjects in Bloomberg, Businessweek ,the Colorado Actual Property Journal, Nationwide Affiliation of Realtors Journal, The Actual Deal actual property information, the CO Biz Journal, The Denver Put up, The Scotsman mortgage dealer information, Mortgage Skilled America and varied different nationwide publications.