{kind=link}

In each article I examine actual property they spotlight that stock is inflicting costs to fall, or excessive rates of interest, or not sufficient demand. All of these things above are solely signs. What’s the actual driver transferring costs as we speak? What does this imply for the rest of the 12 months and into subsequent 12 months?

Signs vs. precise prognosis

When fascinated by actual property, it seems actual property has caught a figurative chilly that means that the market isn’t feeling “good”. Utilizing the chilly analogy we’re seeing numerous signs like rising stock, longer time available on the market, value reductions, and so forth… All of these things describe the consequences of the chilly versus diagnose that you’ve got for instance a sinus an infection. To actually perceive the chilly that actual property has, we should perceive the precise root reason for the signs.

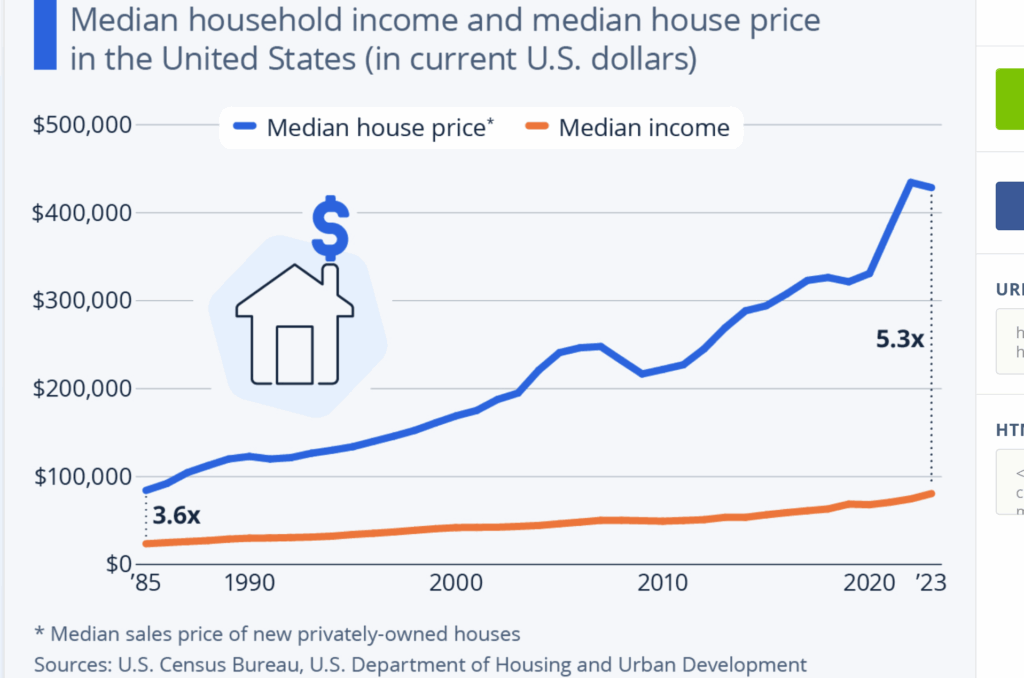

Revenue vs. value

Traditionally home costs had been round 3-4% instances the common revenue. As you possibly can see within the chart above in 1985 the median house value was about 3.6x the median revenue which was thought-about within the wholesome vary. Quick ahead to the current and we’re approaching 5.3 instances revenue.

To place this in perspective. Households incomes $100,000 a 12 months might afford to purchase 37% of the houses listed available on the market in March, based on an evaluation by NAR and Realtor.com. Six years earlier, when mortgage charges and typical house costs had been decrease, a family incomes that very same quantity might afford 65% of obtainable listings. Lengthy and quick revenue isn’t coming even near maintaining with house costs or vice versa the place house costs are rising manner too quick for revenue.

Imbalance between home costs and revenue didn’t matter

Over the past 15 years or so, the imbalance between home costs and revenue principally didn’t matter because of one issue, rates of interest. For instance for those who might borrower at 2.75% regardless that you had been shopping for a way more costly home it wasn’t a difficulty as rates of interest had been so low and have been for therefore lengthy it masked the imbalance between revenue and home costs.

Why did Covid supercharge costs

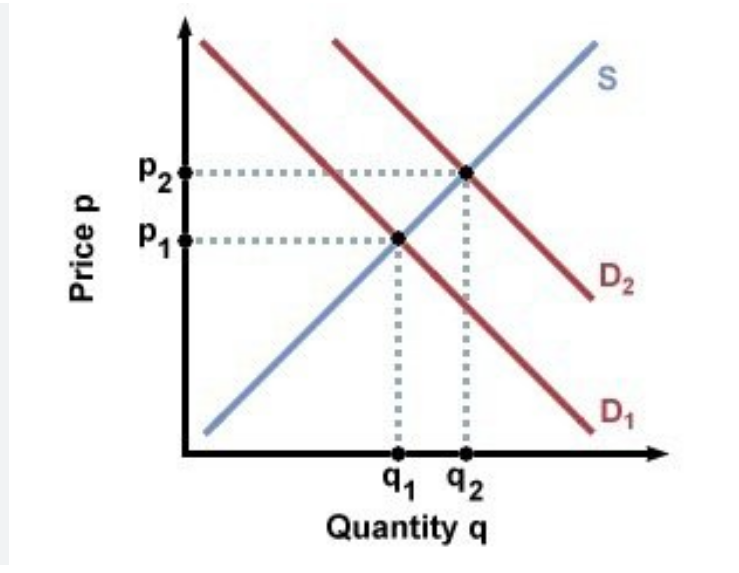

When the federal reserve and the president responded throughout Covid, they launched into one of many greatest quantitative easing experiments. They pumped cash into the financial system by way of direct checks and likewise the federal reserve dropped rates of interest to zero. On prime of that the federal reserve needed to get much more cash into provide so that they started shopping for mortgage bonds/securities to additional push down mortgage charges. This result in traditionally low charges. These low charges in flip spurred much more shopping for of actual property as consumers might afford a lot at 2.75% now. What occurred is fundamental economics illustrated by the chart under the place costs improve because of a surge in demand because of extremely low charges.

Why are we simply now seeing the imbalance of costs and incomes

The imbalance between costs and incomes has been there all alongside, we simply didn’t care as rates of interest lined up the divergence. Quick ahead and we’re in a time interval of upper rates of interest. Word, todays charges are about common over a 50 12 months or so interval, they had been simply traditionally low in Covid and popping out of the 08 recession.

Sadly the place we’re as we speak with charges is about the place they’ll stay for the foreseeable future because of larger authorities deficit spending resulting in larger rates of interest (here’s a extra in depth dialogue on this matter that I wrote about earlier).

Lengthy and quick the conventional rates of interest we’re seeing now have highlighted the massive downside we now have the place incomes haven’t stored up with costs.

Can the federal reserve save the true property market.

Many imagine that the federal reserve can simply swoop in and drop charges to rescue the true property market. Sadly this might not be farther from the reality. Keep in mind the federal reserve solely units very quick time period charges (the federal funds fee) and the “market” units mortgage charges primarily based on the yield of the ten 12 months treasury. Treasury notes now are pushed by enormous provide from deficit spending that doesn’t appear to be getting any higher anytime quickly even with the brand new tax plan. It will result in charges staying about the place they’re even when the federal reserve lowers quick time period charges.

What occurs to actual property costs

The true property market can not stay with costs outpacing incomes in our present rate of interest surroundings and the fed can’t save us. Sadly finally one thing will break which we’re seeing the signs of as we speak. Have a look at this chart for Denver Condos, clearly this market is present process a transition. As demand falls and stock will increase it highlights the signs of the massive disconnect between incomes and costs.

The one manner this market shakes out is both an enormous surge in revenue which is uncertain primarily based on the historic will increase or a big reset in costs which is extra doubtless primarily based on historic knowledge. The opposite state of affairs is that costs keep about the identical for the subsequent 15 years or so for incomes to catch as much as costs which I feel is a good worse final result than a reset in costs. Lengthy and quick, the masking of the disconnect between home costs and revenue goes to return to a head sooner slightly than later.

Extra Studying/Sources

https://www.fairviewlending.com/why-are-mortgage-rates-rising-when-they-should-be-falling/

https://www.fairviewlending.com/2025-mortgage-rate-predictions/

We’re a Colorado Non-public/ Onerous Cash Lender funding in money!

I would like your assist as my aim in writing these articles is to supply the perfect info/perception on Colorado Actual Property that you just can not get wherever else! Please like and share my articles on linked in, twitter, fb, and different social media and ahead to your mates/associates I might tremendously admire it.

Glen Weinberg personally writes these weekly actual property blogs primarily based on his actual property expertise as a lender and property proprietor. He’s the proprietor of Fairview Business Lending. Glen has been printed as an professional in laborious cash lending, actual property valuation, financing, and numerous different actual property subjects in Bloomberg, Businessweek ,the Colorado Actual Property Journal, Nationwide Affiliation of Realtors Journal, The Actual Deal actual property information, the CO Biz Journal, The Denver Publish, The Scotsman mortgage dealer information, Mortgage Skilled America and numerous different nationwide publications.

Glen resides in Colorado, lends in Colorado, owns property in Colorado, and providers loans in Colorado which offers a singular actual property potential of what’s really taking place on the bottom each in Denver and all through Colorado. My aim of this actual property weblog is to supply an trustworthy evaluation of what I see taking place in Colorado actual property and the way it will influence actual property homeowners, consumers, realtors, mortgage professionals, and so forth…

Fairview is the acknowledged chief in Colorado Onerous Cash and Colorado non-public lending specializing in residential funding properties and business properties each in Denver and all through the state. We’re the Colorado specialists having closed 1000’s of loans all through the Entrance vary, Western slope, resort communities, and all over the place in between. We additionally stay, work, and play within the mountains all through Colorado and perceive the intricacies of every market.

While you name you’ll communicate on to the choice makers and get an trustworthy reply rapidly. We’re acknowledged within the business because the chief in Colorado laborious cash lending with no upfront charges or some other video games. Study extra about Onerous Cash Lending by way of our free Onerous Cash Information. To get began on a mortgage all we want is our easy one web page software (no upfront charges or different video games)

Tags: Denver laborious cash, Denver Colorado laborious cash lender, Colorado laborious cash, Colorado non-public lender, Denver non-public lender, Colorado ski lender, Colorado actual property traits, Colorado actual property costs, Non-public actual property loans, Onerous cash loans, Non-public actual property mortgage, Onerous cash mortgage lender, Onerous cash mortgage lender, residential laborious cash loans, business laborious cash loans, non-public mortgage lender, Onerous Cash Lender, Non-public lender, non-public actual property lender, residential laborious cash lender, business laborious cash lender, No doc actual property lender