{kind=link}

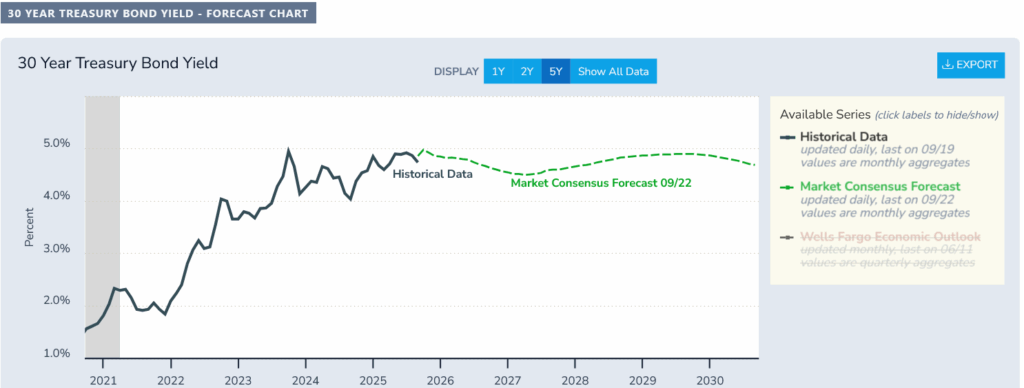

The federal reserve lowers rates of interest and indicators two extra reductions the rest of the 12 months. On the similar time mortgage charges are barely shifting. Why are mortgage charges having such a big disconnect with the Federal Reserve. Will charges proceed to fall or keep the identical or larger? What does this imply for actual property? What excellent news is the chart above exhibiting?

Federal Reserve doesn’t management long-term charges

Though many imagine that the federal reserve “controls” rates of interest, it is a delusion. The Federal Reserve can solely set brief time period charges and the market “controls” long run charges like the ten 12 months treasury or 30 12 months bond. Lengthy and brief, the federal reserves strikes are solely a part of the equation on long run charges. What’s the “market” telling us of the place charges head from right here?

30 12 months bond predicts larger long run charges

Though the 30 12 months bond just isn’t the ten 12 months treasury that’s principally the “peg” for mortgage charges, it does present the long run market expectations for treasuries and in flip mortgage charges. If we have a look at the chart above the newest predictions the bond market is predicting a small little dip after which long run fee will proceed rising. The market could possibly be making these predictions for numerous causes:

- Inflation stays larger: Which means 30 12 months bonds would want to remain excessive/pay a premium to make sure buyers actual {dollars} proceed rising

- Elevated deficits: Elevated deficits trigger and improve in authorities borrowing resulting in a rise within the provide of bonds. As provide will increase, costs fall which results in larger yields (keep in mind treasury costs and charges work in inverse)

I’d agree with the predictions above as there are significantly extra elements influencing long term bond yields to remain considerably larger for longer.

Mortgage fee predictions are mistaken, they are going to be a lot larger for longer

When you have a look at any mainstream actual property publication, rates of interest are predicted to fall effectively beneath the place they’re right now. Sadly, I believe these predictions are lifeless mistaken. To find out the place mortgage charges shall be in 2026 if I lined up the 30 12 months historic chart above together with the historic mortgage chart beneath, it implies that charges shall be similar to the place they had been in 2008 which might put mortgage charges by means of 2026 within the 6.25 to 7% vary which is about the place they’re now.

Even wanting past 2026 charges probably will keep effectively above the extremely low charges from 2009 to 2019 as authorities spending ramps up which can maintain charges significantly larger than the final 10 years.

What do 6% and above charges imply for residential and industrial actual property?

With charges staying larger for longer there shall be large impacts on actual property costs:

Residential: Increased charges finally will result in declining costs particularly in larger priced markets as much less folks can afford to buy costly homes. Assuming a 500k mortgage at a 4% fee precovid the funds could be 2,387/month, now quick ahead and that very same mortgage could be 3160/month. That is an additional 9300/12 months in mortgage funds. This large bounce in funds doesn’t work for many potential patrons which can in the end result in costs falling with a purpose to improve affordability. On the flip facet, primarily based on the lock in impact, the upper for longer can even result in the residential actual property market principally “caught” the place it’s with low volumes as debtors can’t or is not going to quit their low fee.

Industrial: We’ve not even come near seeing the underside within the industrial market. As charges stay larger cap charges can even have to rise which can in the end result in a a lot deeper reset in industrial property values. Billions in mortgages are going to reset over the following few years and for now lenders have kicked the can down the highway however as charges stay larger for longer finally the market should face the music of a lot decrease property values. For instance, I’ve seen workplace buildings buying and selling at 20-30% off their values from just some years in the past. Additionally, you will see an additional reset in multifamily and retail as cap charges are manner too low with treasuries staying larger for longer.

Abstract

The market is lifeless mistaken on the idea that rates of interest will quickly fall anytime quickly and “save” actual property. We’re already seeing this play out right now. Even with the current cuts and predicted ¾% lower the rest of the 12 months rates of interest are principally caught. Sadly, bigger authorities spending and the push for a delicate touchdown resulting in inflation will maintain long run charges like mortgages a lot larger for for much longer than is being priced in. That is clearly proven within the 30 12 months bond yield prediction above.

For the reason that market hasn’t come to phrases with larger for longer, the market is grossly underestimating the impacts to residential and industrial actual property. With mortgage charges above 6% by means of 2026, industrial actual property is primed for a considerable correction as the present costs usually are not sustainable in a better fee surroundings. For instance, why would somebody purchase a industrial property on a 4-5% cap after they should purchase a authorities bond with the identical return with zero danger. Sadly, they might not, which implies costs should alter downward. On the flip facet the residential market will proceed both staying caught or trending barely downward.

Sadly predicting when the reset will happen is difficult as macro elements like a warfare, surge in oil costs, inventory market meltdown, and many others… can occur out of nowhere. With that mentioned, my finest guess is mid 2026 because the market involves grips that low long run charges usually are not going to bail out the actual property market as charges keep larger for longer. On the flip facet, we additionally might keep away from a correction and principally kick alongside in a stagflationary financial system for some time.

Extra Studying/Assets

- https://fred.stlouisfed.org/sequence/MORTGAGE30US

- https://econforecasting.com/forecast/t30y

- https://www.fairviewlending.com/fed-cuts-rates-why-are-mortgage-rates-rising/

- https://www.fairviewlending.com/commercial-real-estate-what-is-causing-the-decline/

- https://www.fairviewlending.com/root-cause-of-real-estate-price-declines/

We’re a Non-public/ Arduous Cash Lender funding in money!

Glen Weinberg personally writes these weekly actual property blogs primarily based on his actual property expertise as a lender and property proprietor. I’m not an armchair reporter/author. We’re an precise personal lender, lending our personal cash. We service our personal loans and personal industrial and residential actual property all through the nation.

My day job is and continues to be personal actual property lending/ exhausting cash lending which allows me to have a novel perspective in the marketplace. I don’t settle for any paid sponsorships or adverts on my weblog to make sure correct data. I’ve been scripting this for nearly 20 years and have over 30k subscribers. Please like and share my blogs on linkedin, twitter, fb, and different social media and ahead to your pals . I’d significantly admire it.

Fairview is a exhausting cash lender specializing in personal cash loans / non-bank actual property loans in Georgia, Colorado, and Florida. We’re acknowledged within the business because the chief in exhausting cash lending/ Non-public Lending with no upfront charges or every other video games. We fund our personal loans and supply sincere solutions rapidly. Study extra about Arduous Cash Lending by means of our free Arduous Cash Information. To get began on a mortgage all we’d like is our easy one web page software (no upfront charges or different video games).

Written by Glen Weinberg, COO/ VP Fairview Industrial Lending. Glen has been revealed as an professional in exhausting cash lending, actual property valuation, financing, and numerous different actual property subjects in Bloomberg, Businessweek ,the Colorado Actual Property Journal, Nationwide Affiliation of Realtors Journal, The Actual Deal actual property information, the CO Biz Journal, The Denver Submit, The Scotsman mortgage dealer information, Mortgage Skilled America and numerous different nationwide publications.

Tags: Arduous Cash Lender, Non-public lender, Denver exhausting cash, Georgia exhausting cash, Colorado exhausting cash, Atlanta exhausting cash, Florida exhausting cash, Colorado personal lender, Georgia personal lender, Non-public actual property loans, Arduous cash loans, Non-public actual property mortgage, Arduous cash mortgage lender, residential exhausting cash loans, industrial exhausting cash loans, personal mortgage lender, personal actual property lender