{kind=link}

Have a look at the chart above of client delinquencies? We at the moment are in keeping with 2017, however is that the actual story? Have a look at 07 what do you discover? Will the economic system mirror the 08 reset or has one thing else essentially modified? With the present delinquency charges are we like 03, 07, or 2017? What’s the greatest guess for when a reset happens?

The significance of delinquency monitoring

As we will see with the chart delinquencies observe a sample, they usually begin small and rise over time, have a look at beginning round 06/07 we noticed delinquencies start to rise modestly after which choose up enormous momentum with a peak round 2010. Basically we bought a sign of what was to return with the rising delinquencies 4 years earlier than issues bought dangerous.

On the flip facet, have a look at 03, delinquencies rose after which fell once more earlier than rising considerably after 06. Basically there was round a 7 12 months interval earlier than delinquencies hit their peak however solely about 5 years earlier than the official recession in 2008.

Lengthy and brief, we don’t know the place we’re within the cycle.

This cycle is completely different than 08 for 3 causes:

Mark Twain famously mentioned that historical past rhymes however doesn’t essentially repeat. At the moment’s cycle is far completely different than 08

- Don’t have the subprime publicity: the set off for the 08 disaster was the subprime disaster the place anybody with a pulse might get a mortgage, defaults rose which finally led to a market meltdown. We should not have that very same threat on this cycle as underwriting is far stricter than prior to now.

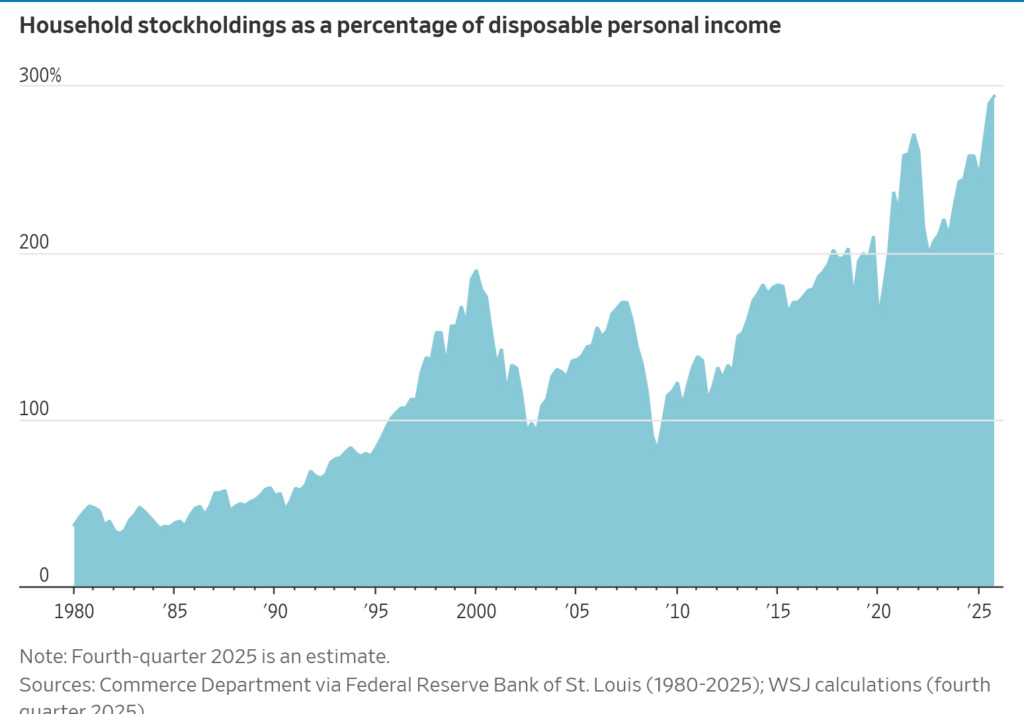

- Have a better focus in shares: Have a look at the chart under. At the moment the inventory market as a proportion of disposable earnings is double what it was in 2008. This implies because the inventory market pulls again from document highs, the wealth impact will trickle down and will simply result in a serious recession a lot faster than 08.

- Debt immediately is larger general than in 08: At the moment the quantity of debt that customers, companies, and the federal government is at a document excessive. This implies when issues get rocky within the economic system there’s a a lot larger probability of a lot bigger issues.

No massive modifications within the economic system are imminent

Based mostly on the charts above, there’s enormous uncertainty of the place we head within the economic system. To additional the confusion, I surveyed readers and requested the query of what occurs within the economic system over the following two years. With an inexpensive margin of error there are equal possibilities of principally each state of affairs from an enormous crash to a roaring economic system.

Massive threat of when economic system modifications a lot worse

Though I can’t predict when the financial winds will shift, I’m extra involved that we might have a a lot worse final result than the markets are pricing in. Client debt, firm debt, and authorities debt are all at information and defaults are growing. We’ve seen in each cycle that in some way debt is the set off. For instance, within the final cycle subprime actual property debt was the fuse that lit the financial cannon resulting in trillions in losses. This cycle, though mortgage debt by way of subprime lending just isn’t as loopy because it was in 08 there are nonetheless threat elements.

For instance, have a look at the federal deficit, there is no such thing as a plan by both social gathering to get debt underneath management which is able to result in larger charges on the whole lot attributable to extra bonds on the market. Moreover, there’s a ton of unsecured client debt like purchase now pay later that has by no means been stress examined. Couple these money owed with firms which have been on a borrowing spree and the dangers to the economic system are amplified.

What does all the info say concerning the economic system?

What occurs subsequent and when is the million greenback query. My intestine says we’re initially of this subsequent cycle. Referencing the chart above this could put 2026 much like 2006/7, however keep in mind the worst impacts didn’t happen till 2010 which suggests we might nonetheless be a number of years away from the height within the subsequent cycle.

Though I don’t know precisely when the economic system will reset, it does give me consolation that the survey outcomes from a month or so in the past additionally expressed enormous ranges of opinions with equal possibilities of principally each chance occurring. No matter when the cycle begins, the large will increase in debt and the uptick in lates/defaults is a warning that the economic system might change swiftly.

I liken our economic system to a ship that’s grossly obese with debt and it might tackle water at any time when the seas turn into uneven. Now’s the time to organize; I might implore everybody to scale back debt to trip by the storm and guarantee you’ve a life jacket, aka ample money, to trip by no matter storm the economic system throws.

Further Studying/Sources

- https://www.bloomberg.com/information/articles/2026-02-10/us-consumer-delinquencies-jump-to-highest-in-almost-a-decade?srnd=homepage-americas

- https://www.fairviewlending.com/what-will-be-the-average-30-year-rate-in-2026/

- https://www.wsj.com/economic system/jobs/capital-labor-wealth-economy-2fcf6c2f?mod=hp_lead_pos3

- https://www.fairviewlending.com/has-the-economy-lost-its-mind/

We’re a Non-public/ Onerous Cash Lender funding in money!

Glen Weinberg personally writes these weekly actual property blogs primarily based on his actual property expertise as a lender and property proprietor. I’m not an armchair reporter/author. We’re an precise personal lender, lending our personal cash. We service our personal loans and personal business and residential actual property all through the nation.

My day job is and continues to be personal actual property lending/ onerous cash lending which allows me to have a novel perspective available on the market. I don’t settle for any paid sponsorships or advertisements on my weblog to make sure correct data. I’ve been scripting this for nearly 20 years and have over 30k subscribers. Please like and share my blogs on linkedin, twitter, fb, and different social media and ahead to your folks 😊. I might tremendously recognize it.

Fairview is a onerous cash lender specializing in personal cash loans / non-bank actual property loans in Georgia, Colorado, and Florida. We’re acknowledged within the business because the chief in onerous cash lending/ Non-public Lending with no upfront charges or some other video games. We fund our personal loans and supply sincere solutions rapidly. Be taught extra about Onerous Cash Lending by our free Onerous Cash Information. To get began on a mortgage all we’d like is our easy one web page utility (no upfront charges or different video games). Be taught the way to discover a respected onerous cash lender and why Fairview is the greatest onerous cash lender for buyers.

Written by Glen Weinberg, COO/ VP Fairview Industrial Lending. Glen has been revealed as an knowledgeable in onerous cash lending, actual property valuation, financing, and numerous different actual property matters in Bloomberg, Businessweek ,the Colorado Actual Property Journal, Nationwide Affiliation of Realtors Journal, The Actual Deal actual property information, the CO Biz Journal, The Denver Publish, The Scotsman mortgage dealer information, Mortgage Skilled America and numerous different nationwide publications.

Tags: Onerous Cash Lender, Non-public lender, Denver onerous cash, Georgia onerous cash, Colorado onerous cash, Atlanta onerous cash, Florida onerous cash, Colorado personal lender, Georgia personal lender, Non-public actual property loans, Onerous cash loans, Non-public actual property mortgage, Onerous cash mortgage lender, residential onerous cash loans, business onerous cash loans, personal mortgage lender, personal actual property lender, residential onerous cash lender, business onerous cash lender, No doc actual property lender