{kind=link}

I noticed a current advert for a Porsche electrical Taycan that was lower than 18 months outdated accessible for half of its authentic price. What can this big drop in costs over a short while inform us about an impending actual property drawback? Why am I even Porsche resale values? What property varieties are most impacted, and can it have an effect on you? What property must you by no means purchase at any worth level?

Why am I even Porsche resale values?

Porsche automobiles present a singular perspective on the financial system. It’s the increased finish of rich discretionary purchases however not out of attain for a lot of rich like a Ferrari or Bently. By watching Porsche, it’s an indicator of the place rich client spending is heading.

What can the Taycan inform us about lease vs Purchase?

The Taycan within the advert caught my consideration. New it books out at 140k and this one lower than 18 months later with solely 6k miles was listed for 70k, half the unique checklist worth. On the flip facet an identical Porsche 718 with comparable specs over the identical 18 months had solely dropped about 15%. It shouldn’t be a shock as know-how in electrical automobiles is altering so quickly it’s exhausting to justify shopping for a brand new Taycan to take a 50% hit in lower than 2 years.

Condos throughout the nation are going through an eerily comparable scenario

As I used to be trying on the particulars on the Taycan, a lightbulb went off that many condos could possibly be going through an identical scenario to the Taycan with big drops in values resulting from fast adjustments available in the market. In essence, in lots of condos it might not be value it to purchase sure items at any worth.

What’s going on within the apartment market?

Condominium house owners throughout the nation are going through a paralyzing drawback: They’ll’t promote their properties due to a fast-growing and largely secret mortgage blacklist. Don’t fear this isn’t some loopy conspiracy from the federal government. I’ve skilled this primary hand on a number of condos in Georgia, Colorado, and Florida.

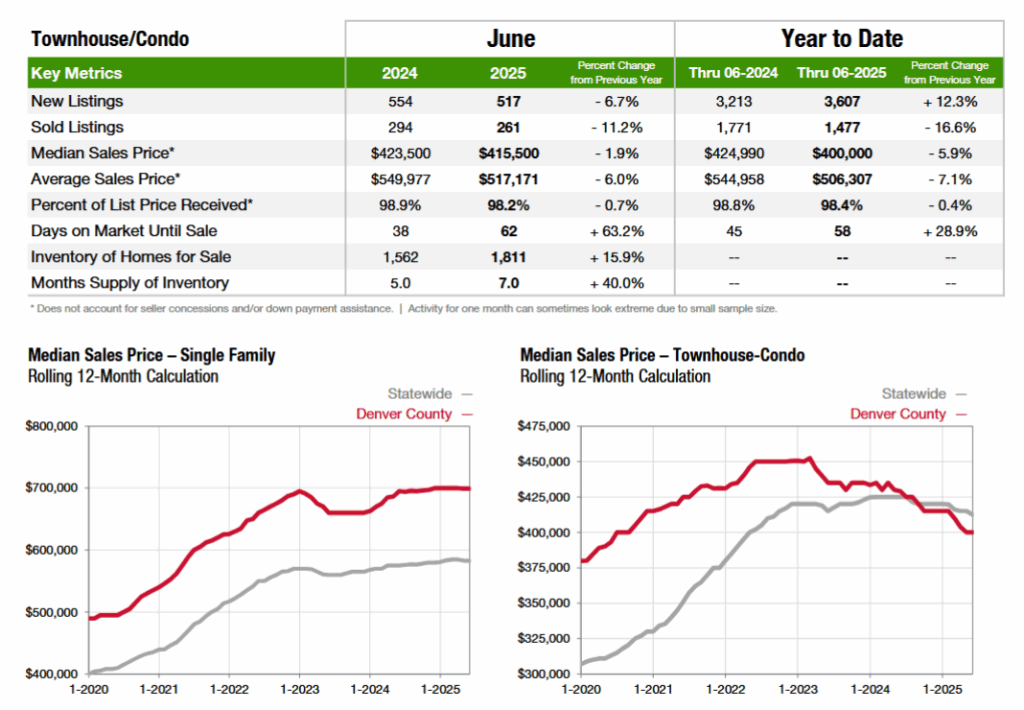

Have a look at the information above from 24 to 25 in Denver and you’ll see this starting to play out with declining values and big jumps in stock up 33% yr over yr together with a decline in closings. This can be a dangerous scenario that’s solely going to worsen.

What was within the information on blacklisted condos?

The blacklist is maintained by Fannie Mae and consists of apartment associations that the mortgage finance big thinks don’t have enough property insurance coverage or have to make vital constructing repairs. Being on the checklist could make it more durable for potential patrons to get a mortgage.

The variety of properties that fail to fulfill Fannie Mae’s requirements has risen to five,175 this month from just a few hundred earlier than Surfside.

Why the large change in blacklisted condos?

Fannie Mae and sister group Freddie Mac don’t make loans, however purchase roughly half of the nation’s house loans from lenders and package deal them to promote to buyers, then assure funds on them. Loans that meet Fannie or Freddie’s underwriting requirements, referred to as conforming loans, may be cheaper and require decrease down funds than bespoke mortgages.

To make sure the debt may be repaid ought to the property be broken or destroyed, Fannie and Freddie have lengthy required a minimal stage of insurance coverage protection for house loans they’re keen to purchase.

Final yr, the companies issued clarifications of those pointers, detailing coverage no-nos which have prompted lenders to take a stricter line on insurance coverage necessities, in response to lenders, real-estate brokers and insurers.

A spokeswoman for Fannie mentioned its necessities are designed to “assist shield debtors from bodily unsafe or financially unstable initiatives.” She disagreed with characterizing Fannie’s database of initiatives, which incorporates properties that each do and don’t meet its lending standards, as a blacklist. She mentioned the agency gives a web-based instrument that enables lenders to test whether or not it accepts loans from a given undertaking.

What two components led to Condos getting on the blacklist?

There are two components Fannie/Freddie take a look at to find out if a apartment is appropriate for financing:

- Upkeep/Reserves: After the apartment collapse in FL just a few years in the past and new legal guidelines in lots of states, many complexes have discovered themselves severely underfunded for routine upkeep and anticipated bills for roofs, foundations, elevators, hvac, and many others…

- Insurance coverage: Many apartment complexes don’t carry full substitute price on insurance coverage as required by Fannie/Freddie. One purpose for the leap in insurance coverage prices: Insurers now need to pay for the depreciated worth of a broken roof, moderately than the complete substitute price, a characteristic Fannie and Freddie oppose. Many insurers additionally need to elevate deductibles increased than Fannie or Freddie permit.

- Loads of associations are attempting to scale back hovering insurance coverage charges by agreeing to pared-down insurance policies that may make their condos ineligible for mortgages backed by Fannie and Freddie. Some owners’ gross sales are falling by way of, and others are on the lookout for patrons who will pay money or get different kinds of loans.

- Shadow Ridge, a Los Angeles complicated blacklisted in December, is in a brushfire zone however escaped this yr’s infernos. Its house owner’s affiliation was not too long ago quoted $2.6 million a yr for a Fannie-compliant coverage, 10 occasions the present price, in response to Jinah Kim, one of many board members.

What occurs when a apartment undertaking is on the mortgage blacklist?

I’ve seen just a few eventualities play out for condos which are unable to get standard financing from Fannie/Freddie:

- Improve down cost: I’ve seen a number of events the place a lender would settle for the mortgage with a down cost of 30-35% versus 20% or much less relying on the lender. The problem is most of the complexes which have points are reasonably priced and debtors cannot afford a 35% down cost or they’d be a home or different property.

- Discover one other lender with increased charges: On just a few events I’ve seen different lenders in a position to step in to finance albeit at increased charges.

- Can’t get financing: Some condos are unable to get financing at any stage which results in all money gross sales

No matter which state of affairs above performs out, every one results in a lot decrease resale values. I’ve seen costs dropped from 10% to nearly 40% if it needs to be an all money buy. Should you personal a apartment or are a apartment in a blacklisted complicated financing will probably be harder and or could possibly be non existent.

Some apartment complexes will develop into mainly nugatory

I’ve seen this a number of occasions on apartment complexes all through the nation the place the items develop into mainly nugatory because the insurance coverage and prices to replace vital objects outweigh the worth of the items. That is very true in decrease priced apartment complexes

Many low-priced apartment complexes are not viable

Decrease priced apartment complexes will probably be hit the toughest as residents can’t incur big jumps in dues wanted for insurance coverage and upkeep. This concern has been a very long time coming as many complexes stored HOA dues as little as doable to help residents however now, they’ve big monetary points which have compounded.

Large adjustments forward within the apartment market

It’s unlucky that many decrease priced condos are not viable. Traditionally, somebody might purchase a apartment, construct some fairness after which transfer into the single-family market. Now with home costs leaping all through the nation whereas apartment costs are slumping the power to maneuver up is shortly being erased.

Abstract

It’s loopy, on the duvet of the article is a Porsche that books at 140k which is a starter apartment in lots of markets. Sadly, the market in electrical automobiles and condos has shifted on a dime the place it’s not viable to purchase a decrease priced apartment as the danger from particular assessments for upkeep and insurance coverage make the monetary calculation perilous. Simply as we see within the electrical automobile market, it’s considerably cheaper to lease versus purchase, that very same equation is now true for a lot of decrease priced condos no matter how low cost they’re in comparison with a single-family house.

The unlucky half is that because the apartment market adjustments, the trail to house possession is radically altered because the entry level to purchase is now a lot increased and a lot farther out of attain for first time patrons.

Further studying/sources

https://www.fairviewlending.com/property-insurance-rates-set-to-jump-by-50-why-and-who-pays/

https://coloradohardmoney.com/condo-prices-fall-throughout-colorado/

https://www.wsj.com/finance/regulation/condo-sales-home-insurance-crisis-a921362b?mod=mhp

We’re a Personal/ Exhausting Cash Lender funding in money!

Glen Weinberg personally writes these weekly actual property blogs based mostly on his actual property expertise as a lender and property proprietor. I’m not an armchair reporter/author. We’re an precise non-public lender, lending our personal cash. We service our personal loans and personal industrial and residential actual property all through the nation.

My day job is and continues to be non-public actual property lending/ exhausting cash lending which allows me to have a singular perspective available on the market. I don’t settle for any paid sponsorships or adverts on my weblog to make sure correct data. I’ve been scripting this for nearly 20 years and have over 30k subscribers. Please like and share my blogs on linkedin, twitter, fb, and different social media and ahead to your folks . I’d vastly admire it.

Fairview is a exhausting cash lender specializing in non-public cash loans / non-bank actual property loans in Georgia, Colorado, and Florida. We’re acknowledged within the trade because the chief in exhausting cash lending/ Personal Lending with no upfront charges or some other video games. We fund our personal loans and supply trustworthy solutions shortly. Be taught extra about Exhausting Cash Lending by way of our free Exhausting Cash Information. To get began on a mortgage all we want is our easy one web page software (no upfront charges or different video games).

Written by Glen Weinberg, COO/ VP Fairview Industrial Lending. Glen has been printed as an knowledgeable in exhausting cash lending, actual property valuation, financing, and varied different actual property matters in Bloomberg, Businessweek ,the Colorado Actual Property Journal, Nationwide Affiliation of Realtors Journal, The Actual Deal actual property information, the CO Biz Journal, The Denver Put up, The Scotsman mortgage dealer information, Mortgage Skilled America and varied different nationwide publications.

Tags: Exhausting Cash Lender, Personal lender, Denver exhausting cash, Georgia exhausting cash, Colorado exhausting cash, Atlanta exhausting cash, Florida exhausting cash, Colorado non-public lender, Georgia non-public lender, Personal actual property loans, Exhausting cash loans, Personal actual property mortgage, Exhausting cash mortgage lender, residential exhausting cash loans, industrial exhausting cash loans, non-public mortgage lender, non-public actual property lender, residential exhausting cash lender, industrial exhausting cash lender, No doc actual property lender