{kind=link}

The Biden Administration took steps to allow much less credit-worthy debtors to qualify for mortgages to assist the housing market. Now the Trump workforce is doing much more within the title of boosting dwelling possession and reducing prices for debtors with a shocking twist that can turbocharge threat. Able to “store” for the perfect credit score rating? Does a cellphone now qualify you for a no down fee mortgage? Who pays when issues don’t work out as deliberate?

The brand new Trump proposal to vary credit score scoring

Enter Federal Housing Finance Company (FHFA) director Invoice Pulte, who introduced Tuesday that Fannie and Freddie might start to ensure mortgages based mostly on credit score scores generated by the agency VantageScore. “My ORDER right now (due to my boss, POTUS) will permit for Individuals to make use of their RENT to qualify for a mortgage,” he tweeted.

On the floor, altering the credit score scoring mannequin doesn’t sound like a serious change, however as I dug deeper, a profound shift is going on. VantageScore promotes its scoring mannequin as extra “inclusive” than FICO as a result of it incorporates hire, utility and telecom fee histories. This implies youthful and lower-income individuals who not often borrow or use a bank card can nonetheless get good scores. VantageScore says its credit score mannequin might permit 5 million extra potential homebuyers to qualify for loans.

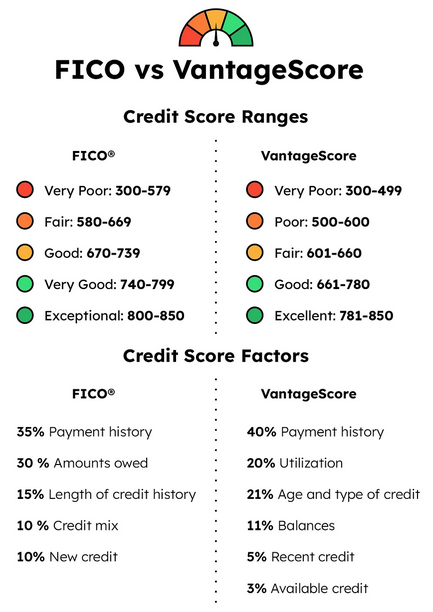

Vantagescore vs Fico

Vantagescore promotes itself as extra inclusive in an effort to develop credit score scores with little or no knowledge.

FICO: Requires at the least six months of credit score historical past to generate a rating.

VantageScore: Can generate a rating with as little as one month of credit score historical past, making it probably helpful for these with restricted credit score historical past. Moreover, the fee historical past might embrace hire, utility funds, and so forth…

Why care a couple of change in credit score scoring fashions?

The massive threat is that mortgage lenders will depend on VantageScore’s scores to qualify marginal debtors and make riskier loans. The left-leaning City Institute final 12 months discovered that VantageScore’s scores on common had been larger than FICO’s. Moreover, the information utilized by VantageScore is significantly completely different. For instance a automotive fee on time over an extended time frame is rather more necessary to credit score worthiness than a cellphone invoice for one month. Underneath VantageScore debtors with just for instance a cellphone invoice or a utility invoice might obtain excessive credit score scores.

Moreover the VantageScore offers a ten% much less weight to utilization. In each cycle we’ve seen the extra leveraged you’re the larger the default charge is. Lengthy and quick VantageScore is permitting significantly riskier debtors to obtain excessive credit score scores and in flip get mortgages which might be finally backed by each taxpayer if there’s a default.

VantageScore utilization will lead to larger mortgage defaults

The Authorities is already enjoying with hearth in actual property offering loans with as little 3.5% down. With the brand new VantageScore, somebody theoretically who solely has a cellphone invoice that they’ve paid on for a month would have a rating excessive sufficient to qualify for an FHA mortgage with solely 3.5% down. Moreover, that very same borrower might negotiate in order that the vendor credit them 3.5% at closing for “repairs”. Now the borrower is placing nothing down.

The riskiness to taxpayers is off the charts and can result in an enormous uptick in defaults. Couple this new program with the height of an actual property market and the outcomes shall be catastrophic.

Massive twist that turbocharges credit score threat, searching for credit score

FHFA, the group that controls Fannie and Freddie that buys virtually all conforming mortgages originated within the US, information that the nonprofit Housing Coverage Council obtained not too long ago by means of a Freedom of Info Act request—first submitted in July 2023—confirmed that officers at Fannie and Freddie had opposed permitting lenders to make use of VantageScore.

A minimum of the Biden FHFA required lenders to undergo Fannie and Freddie each a FICO and VantageScore for all loans. Mr. Pulte, nevertheless, introduced final summer time to a lot fanfare that lenders could be allowed to decide on which rating to make use of when underwriting mortgages. The top of this story writes itself.

Lenders will all the time select the upper rating to allow them to make extra mortgages to dangerous debtors—and at decrease charges. Fannie and Freddie cost larger charges to insure mortgages for debtors with decrease credit score scores. Which means Fannie and Freddie will assure riskier mortgages and cost much less for doing so.

“As a result of FHFA explicitly permits ‘rating buying,’ lenders, realtors, and debtors might merely select the extra favorable rating, resulting in extra approvals, looser credit score, and higher default threat, whereas leaving susceptible debtors with unsustainable debt. Rating suppliers, in flip, could decrease their standards to win extra enterprise,” the AEI researchers clarify.

Chesapeake Threat Advisors’ Clifford Rossi estimates that severe-delinquency charges might improve by 18%. The consulting agency Milliman predicts default charges will rise by some 30%. The American Enterprise Institute’s Ed Pinto, Tobias Peter and Sissi Li estimate assure charges will fall by 10% to 13%, placing taxpayers at higher threat.

Lengthy and quick, credit score scores will grow to be a ineffective predictor of threat as debtors will all the time choose the best rating, on this case VantageScore, however I can assure that FICO will quickly emulate VantageScore or they are going to be out of enterprise.

How will utilizing loosening credit score scores play out in actual life, take a look at photo voltaic bonds

Ove the previous 10 years or so fintech firms have been utilizing different strategies to qualify debtors for loans. That is much like what VantageScore is aiming to do. To see what occurs in actual life, we are able to take a look at the worth of bonds tied to rooftop photo voltaic. The fintech firms targeted on rooftop photo voltaic installations and offered bonds on Wall Avenue. We now have some knowledge on what occurs after the mud settles and it’s not fairly. A few of the bonds offered at the moment are buying and selling at 40 cents on the greenback that means the market is factoring in that they could get again at most 50 cents on each greenback invested. Primarily the photo voltaic bonds have misplaced 60% of their worth as there are questions on compensation of the loans.

The identical factor will occur with mortgages utilizing VantageScore coupled with a low downpayment mortgage. We noticed within the final cycle that defaults elevated based mostly on fairness. This identical development shall be turbocharged with even much less creditworthy debtors.

Turbocharged credit score scores and hovering defaults

On the floor, altering a scoring mannequin shouldn’t be monumental, however as I learn and realized extra, the fact is way completely different. As soon as I take a look at the main points it’s shortly obvious that the federal authorities is establishing one other subprime sort of catastrophe we noticed in 2008. Moreover the race to the best rating for shoppers is turbocharged with the brand new requirement to solely choose the best rating.

Utilizing a brand new scoring mannequin that permits good credit score scores with just one month of fee historical past on gadgets like a cellphone is a recipe for catastrophe. While you couple inflated credit score scores with low downpayment loans whereas on the peak in the true property market a catastrophe is sooner or later. Though we don’t know when the reset will happen the losses shall be extraordinary. Primarily the federal government will turbocharge housing within the quick time period main to large defaults over the long run and a doable repeat of the 08 mortgage debacle.

If we take a look at what is going on on photo voltaic bonds buying and selling at 40 cents on the greenback taxpayers are going to be on the hook for some large losses. The unhappy half is that the federal authorities needs to be doing simply the alternative at this stage in the true property cycle by growing credit score scores and together with requiring larger downpayments in an effort to mitigate threat on the high of the market. Sadly, on the finish of the day it will result in large losses for taxpayers, finally larger deficits, and larger rates of interest for everybody else.

Extra Studying/Assets

We’re a Non-public/ Arduous Cash Lender funding in money!

Glen Weinberg personally writes these weekly actual property blogs based mostly on his actual property expertise as a lender and property proprietor. I’m not an armchair reporter/author. We’re an precise non-public lender, lending our personal cash. We service our personal loans and personal industrial and residential actual property all through the nation.

My day job is and continues to be non-public actual property lending/ onerous cash lending which allows me to have a singular perspective available on the market. I don’t settle for any paid sponsorships or advertisements on my weblog to make sure correct data. I’ve been penning this for nearly 20 years and have over 30k subscribers. Please like and share my blogs on linkedin, twitter, fb, and different social media and ahead to your mates 😊. I’d vastly recognize it.

Fairview is a onerous cash lender specializing in non-public cash loans / non-bank actual property loans in Georgia, Colorado, and Florida. We’re acknowledged within the trade because the chief in onerous cash lending/ Non-public Lending with no upfront charges or some other video games. We fund our personal loans and supply trustworthy solutions shortly. Be taught extra about Arduous Cash Lending by means of our free Arduous Cash Information. To get began on a mortgage all we’d like is our easy one web page utility (no upfront charges or different video games).

Written by Glen Weinberg, COO/ VP Fairview Industrial Lending. Glen has been revealed as an knowledgeable in onerous cash lending, actual property valuation, financing, and varied different actual property subjects in Bloomberg, Businessweek ,the Colorado Actual Property Journal, Nationwide Affiliation of Realtors Journal, The Actual Deal actual property information, the CO Biz Journal, The Denver Put up, The Scotsman mortgage dealer information, Mortgage Skilled America and varied different nationwide publications.

Tags: Arduous Cash Lender, Non-public lender, Denver onerous cash, Georgia onerous cash, Colorado onerous cash, Atlanta onerous cash, Florida onerous cash, Colorado non-public lender, Georgia non-public lender, Non-public actual property loans, Arduous cash loans, Non-public actual property mortgage, Arduous cash mortgage lender, residential onerous cash loans, industrial onerous cash loans, non-public mortgage lender, non-public actual property lender, residential onerous cash lender, industrial onerous cash lender, No doc actual property lender