{kind=link}

Money-out refinancing lets you leverage your property’s fairness to take out a mortgage and might help debtors rapidly entry money and negotiate decrease rates of interest. Earlier than making use of for cash-out refinancing, think about your fairness and new mortgage phrases and charges.

Whether or not you’re a home-owner or actual property investor, having access to the funds you could accomplish your monetary objectives might be tough. You could not qualify for a conventional mortgage resulting from your credit score rating, revenue, and different elements.

The excellent news is there are answers. Money-out refinancing is one solution to leverage your property fairness to get the cash you want for something from a medical emergency to a big buy.

Earlier than making use of for a cash-out refinancing dwelling mortgage, it’s important to grasp the professionals and cons and examine your mortgage choices. Learn on to study cash-out refinancing, the way it works, and whether or not it’s best for you.

- What’s cash-out refinancing?

- How does cash-out refinancing work?

- Eligibility necessities for cash-out refinancing

- How cash-out refinancing differs from different refinancing choices

- Professionals and cons of cash-out refinancing

- What to think about earlier than making use of for cash-out refinancing

- Money-Out Refinancing: FAQs

- Is cash-out refinancing best for you?

What’s cash-out refinancing?

Money-out refinancing helps you to refinance your mortgage to show your property fairness into money you’ll be able to entry. Once you apply for cash-out refinancing, you should utilize a few of the funds you obtain to repay your current mortgage and preserve the remaining as one lump sum. In contrast to the cash you borrow via different mortgage packages, you should utilize the cash from cash-out refinancing for any goal.

How does cash-out refinancing work?

Money-out refinancing could sound advanced, but it surely’s truly a fairly easy course of. Once you apply for cash-out refinancing, you utilize your property fairness to repay your mortgage and take out a brand new mortgage. After paying off your current mortgage, the remaining quantity can be given to you as a lump sum.

Conventional mortgage refinancing lets you refinance to alter your rate of interest and mortgage phrases. Whereas these phrases usually change with cash-out refinancing, it presents the additional benefit of permitting you to make use of the cash you borrow for any goal.

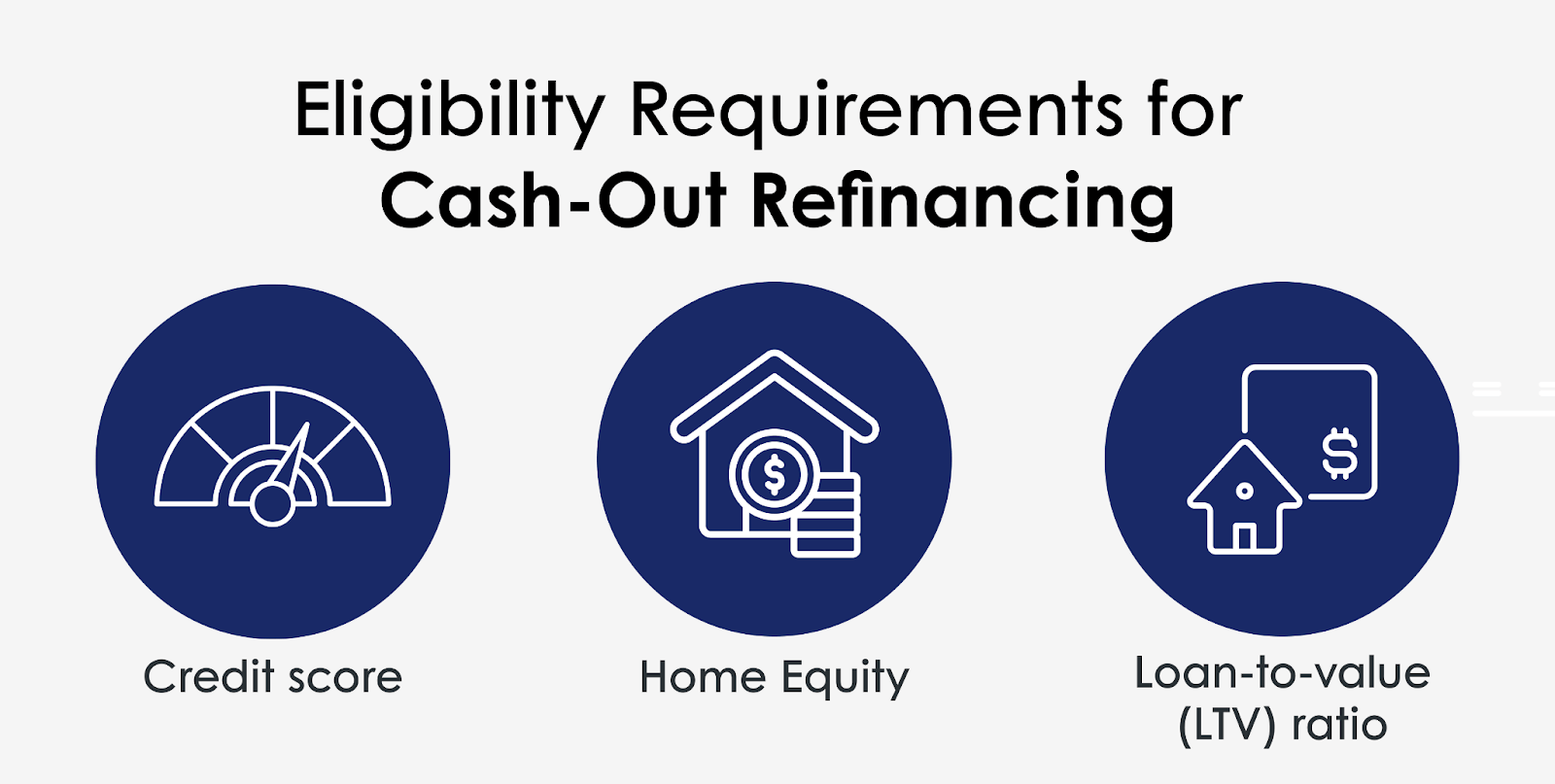

Eligibility necessities for cash-out refinancing

Earlier than you apply for cash-out refinancing, you could meet the overall eligibility necessities. Listed below are the necessities you could meet to be eligible for a cash-out refinance:

- Credit score rating: Lenders look at your credit score rating and historical past to make sure you’re a low-risk borrower. In case your credit score rating is just too excessive or you’ve gotten delinquent accounts, you might not qualify for a mortgage.

- Residence fairness: Your property fairness determines whether or not you’re eligible for a cash-out refinance, and most lenders need you to have no less than 20-30% fairness in your house.

- Mortgage-to-value (LTV) ratio: The LTV ratio is the proportion of an asset’s buy value that’s coated by a mortgage. If you happen to obtain a mortgage of $50,000 to buy a $100,000 asset, the LTV ratio is 50%.

How cash-out refinancing differs from different refinancing choices

Along with cash-out refinancing, you should utilize different forms of loans and refinancing choices to leverage your property fairness. Let’s look at how these refinancing choices examine to cash-out refinancing.

Charge-and-term refinancing is an possibility for householders who need higher mortgage phrases. You’re not taking a mortgage out primarily based on your property fairness — as a substitute, you’re merely negotiating decrease rates of interest, a shorter mortgage time period, or each.

A house fairness mortgage is one other solution to borrow cash by leveraging your property fairness. Your mortgage quantity can be decided by the worth of your property and the way a lot fairness you’ve gotten in it. You’ll be able to select between a conventional dwelling fairness mortgage or a house fairness line of credit score (HELOC), which capabilities like a bank card.

There are numerous different forms of loans you’ll be able to apply for as an actual property investor, together with repair and flip loans and exhausting cash loans for rental properties.

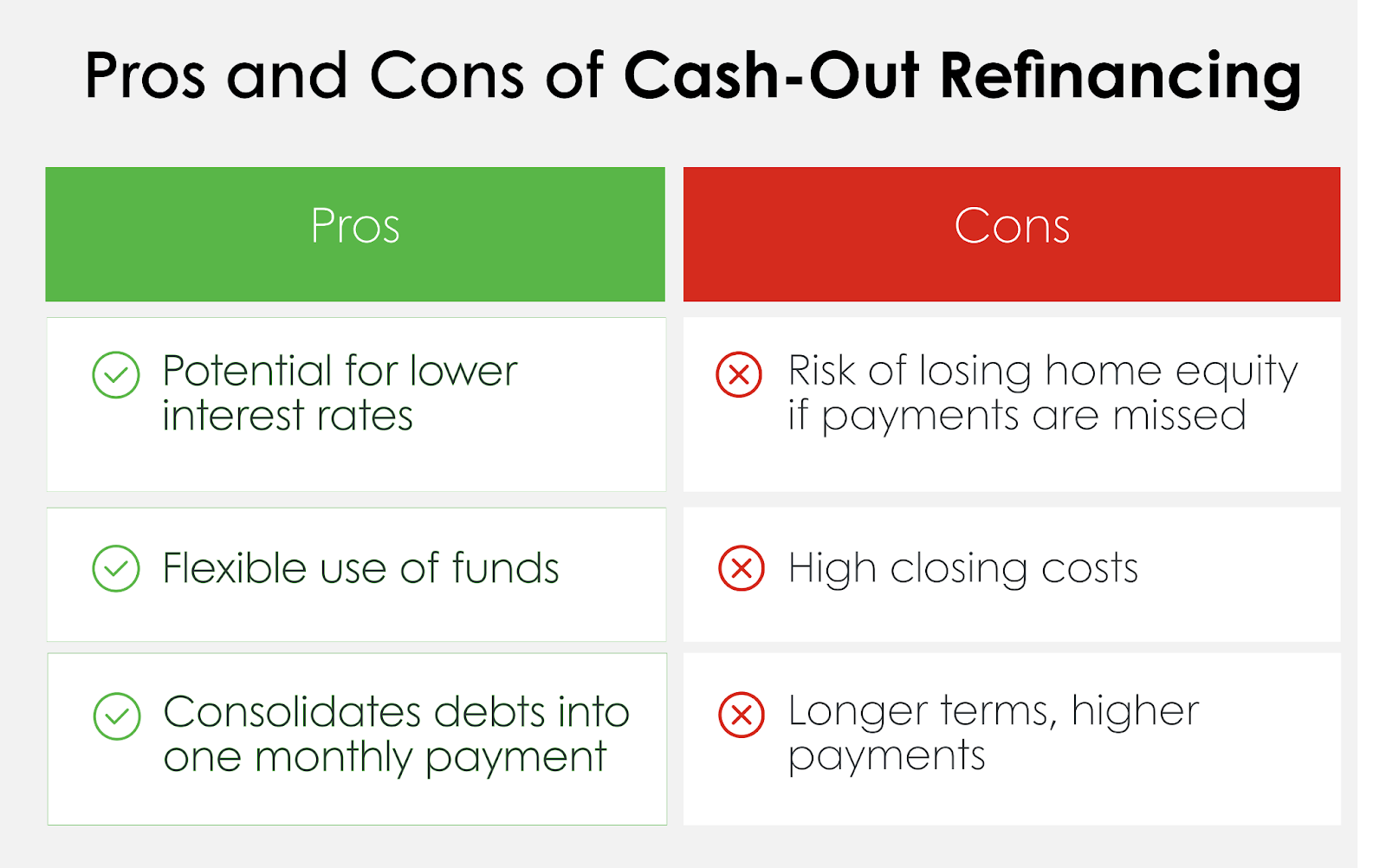

Professionals and cons of cash-out refinancing

Earlier than you apply for cash-out refinancing, it’s vital to grasp the professionals and cons in comparison with different refinancing and exhausting cash mortgage choices. Unsure if a cash-out refinance is best for you? Take a look at a few of the advantages and downsides under.

Professionals

- Money-out refinancing could provide decrease rates of interest than different forms of loans, saving you cash in the long run.

- If you wish to consolidate a number of forms of debt right into a single fee, you’ll be able to repay your debt with cash-out refinancing and make a single month-to-month fee.

- Funds from cash-out refinancing aren’t designated for a particular goal, so you should utilize them for dwelling renovations, emergency payments, or main purchases.

Cons

- You’re placing your property fairness in danger for those who don’t make on-time funds in the course of your mortgage time period.

- Whereas a rate-and-term refinance helps you decrease your month-to-month funds and get your mortgage paid off quicker, cash-out refinancing may end up in longer mortgage phrases and better month-to-month funds.

- Money-out refinancing comes with probably costly closing prices, so ensure you think about these extra prices.

What to think about earlier than making use of for cash-out refinancing

Making use of for any sort of mortgage or refinancing is an enormous determination. Once you’re making main monetary choices, it’s vital to think about your present monetary scenario and long-term objectives earlier than taking motion.

Present market situations can have a big influence on cash-out refinancing. Money-out refinance charges change as market situations change, and the worth of your property may improve or lower relying on the housing market. Take into account consulting an professional to determine how present market situations are affecting cash-out refinances.

Your monetary objectives are one other vital issue to think about. What are your long-term monetary objectives? How are you planning on utilizing the cash out of your cash-out refinance? Consolidating debt could also be a wise transfer, however you would possibly need to rethink for those who’re fascinated with refinancing with a cash-out to fund a serious buy.

Final however not least, think about your future housing plans. Since cash-out refinancing can prolong your mortgage time period, you need to make sure you’re comfy staying in your house for some time. If you wish to buy a brand new dwelling or relocate to a different state, a cash-out refinance in all probability isn’t best for you.

Finally, it’s as much as you to find out whether or not cash-out mortgage refinancing is best for you.

Money-Out Refinancing: FAQs

What’s the most quantity I can borrow?

Once you apply for a cash-out refinancing dwelling mortgage, lenders decide your most mortgage quantity primarily based on your property fairness and loan-to-value ratio. Because of this the utmost quantity you’ll be able to borrow will fluctuate relying in your scenario. You’ll be able to speak to a lender or apply for a mortgage to find out how a lot you’ll be able to borrow.

How lengthy does the cash-out refinancing course of take?

Whereas cash-out refinancing isn’t fairly as fast as some mortgage packages, it doesn’t take lengthy to get authorised for a mortgage and get entry to your cash. Typically talking, you’ll be able to anticipate the whole course of to take between 30 and 60 days. You could obtain your verify the identical day you shut your mortgage, however it might take up to some enterprise days.

Will I have to pay taxes on the money I obtain?

Despite the fact that you usually must pay taxes on lump sums of money you obtain, that’s not the case with a cash-out refinance. Since cash-out refinances are thought of loans, they’re not taxable. Meaning you don’t have to fret about setting any cash apart, so that you’re free to spend the funds you obtain nonetheless you need to spend them.

What’s the distinction between dwelling fairness loans and cash-out refinancing?

A house fairness mortgage is a second mortgage, which implies it creates an extra mortgage on high of your mortgage mortgage. Once you take out a house fairness mortgage, you could make month-to-month funds on that mortgage and your mortgage. With cash-out refinancing, your current mortgage is paid off, so that you solely must cope with one mortgage.

Is cash-out refinancing best for you?

Whether or not you need to consolidate current debt or get entry to emergency funds, cash-out refinancing might help. Earlier than you apply for a cash-out refinance, be sure it’s the appropriate determination primarily based in your monetary scenario.

At Supply Capital, we make it straightforward to qualify for cash-out refinancing so you may get the cash you could take management of your funds. We’ve simplified the cash-out refinancing course of with no prepayment penalties and aggressive rates of interest. With same-day approvals, you don’t have to attend weeks to see in case your software is authorised.

Are you fascinated with utilizing cash-out refinancing to leverage your property fairness? Supply Capital might help. Apply now or contact us to be taught extra about cash-out refinancing and the way it works.