{kind=link}

Mortgage to worth (LTV) is a quantity lenders use to resolve in the event that they need to offer you a mortgage for a home or different property. It’s a share that exhibits how a lot of the home’s worth you’re borrowing. If this quantity is comparatively low, it means you’re borrowing much less in comparison with what the home is value, which lenders choose as a result of it reduces their threat.

When contemplating taking out a mortgage, particularly for one thing vital like shopping for a house or an funding property, you may come throughout varied phrases that may initially appear a bit complicated. One such time period is mortgage to worth. It’s an important idea that may influence the quantity of mortgage you’ll be able to safe and the rate of interest you’ll be supplied.

Understanding how lenders consider threat and decide mortgage quantities may help you make higher monetary selections. Preserve studying to find out about mortgage to worth, the way it’s calculated, and why it’s necessary.

- What’s Mortgage to Worth?

- The way to Calculate Mortgage to Worth

- What’s a Good Mortgage to Worth Ratio?

- Advantages of a Good LTV

- The way to Decrease Your LTV

- Mortgage to Worth: FAQs

- Exhausting Cash Loans with Quick & Simple Approvals

What’s Mortgage to Worth?

Mortgage to worth is a lending metric used to evaluate the lender’s stage of threat once they present a mortgage. This quantity is actually the share that tells you the ratio between the mortgage quantity and the appraised worth of the property or asset being financed.

Lenders use your mortgage to worth ratio to calculate how a lot to lend and to set the phrases of the mortgage, together with the rate of interest, down fee requirement, and the necessity for mortgage insurance coverage. The next LTV means you’ll want a better mortgage quantity, which ends up in extra threat for the lender. If a borrower defaults, the lender might wrestle to recoup their funding by means of the sale of the asset.

Alternatively, a decrease mortgage to worth ratio means the borrower has extra fairness, which reduces the lender’s potential losses if the property worth declines.

Lenders typically have most LTV thresholds for various mortgage varieties.

What’s Mixed Mortgage to Worth?

Whereas understanding the essential mortgage to worth ratio is essential, typically you could hear lenders use the time period mixed mortgage to worth (CLTV). This idea is especially necessary when you’ve a number of loans on a single property.

Mixed mortgage to worth determines the entire worth of all loans on a property in relation to its appraised worth. Not like the usual mortgage to worth ratio, which solely considers the first mortgage, CLTV consists of the first mortgage in addition to any further loans secured by the property. This will likely embody a second mortgage or a house fairness line of credit score (HELOC).

Lenders use CLTV alongside the usual mortgage to worth ratio to evaluate threat and make lending selections, particularly when contemplating further financing on a property with an current mortgage.

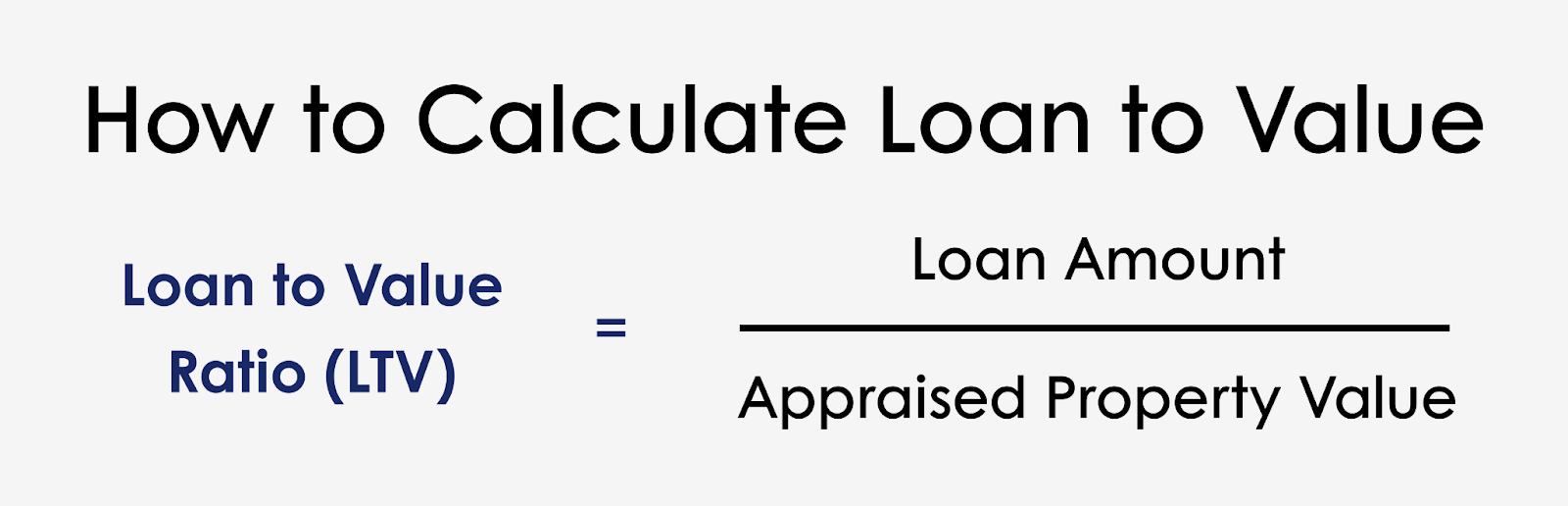

The way to Calculate Mortgage to Worth

The system for calculating mortgage to worth is:

Mortgage to worth = (mortgage quantity / appraised worth of asset) x 100%

Right here’s a breakdown of every element:

- Mortgage quantity: That is the entire amount of cash you borrow from the lender.

- Appraised worth of asset: That is the present market worth of the property or asset as decided by an expert appraiser.

- The result’s multiplied by 100 to specific the ratio as a share.

Let’s say you need to buy a house valued at $300,000, and also you’re in search of a mortgage of $240,000.

- Mortgage quantity: $240,000

- Appraised worth of asset: $300,000

- Mortgage to worth = ($240,000 / $300,000) x 100

- Mortgage to worth = 0.80 x 100

- Mortgage to worth = 80%

An LTV of 80% means you’re borrowing 80% of the house’s worth and offering a 20% down fee.

The way to Calculate Mixed Mortgage to Worth

Calculating the mixed mortgage to worth ratio is much like normal LTV. The one distinction is that you just’re combining all loans related to the property. The system for calculating CLTV is:

CLTV = (sum of all mortgage balances / appraised property worth) x 100%

Breaking this down:

- The sum of all mortgage balances: This consists of the first mortgage and any further loans or traces of credit score secured by the property

- Appraised property worth: The present market worth of the property

- The result’s multiplied by 100 to specific the ratio as a share.

For instance, let’s say you’ve a property appraised at $400,000 with the next loans:

- Major mortgage: $300,000

- Residence fairness line of credit score: $50,000

- CLTV = ($300,000 + $50,000) / $400,000 x 100%

- CLTV = $350,000 / $400,000 x 100%

- CLTV = 0.875 x 100%

- CLTV = 87.5%

On this instance, the mixed mortgage to worth ratio is 87.5%, which suggests the entire of all loans in opposition to the property is 87.5% of its appraised worth.

What’s a Good Mortgage to Worth Ratio?

What’s thought-about a superb mortgage to worth ratio relies on the lender and mortgage kind. For typical and bridge loans, a mortgage to worth ratio of 80% or decrease is usually thought-about good. Because of this the mortgage quantity is 80% or much less of the property’s appraised worth.

This decrease mortgage to worth ratio (or 20% down fee) typically permits debtors to keep away from non-public mortgage insurance coverage (PMI) and will qualify them for higher rates of interest.

Nevertheless, what’s thought-about a superb mortgage to worth ratio can differ for varied mortgage varieties:

- FHA loans: With these loans, you can also make a down fee as little as 3.5%, permitting for a mortgage to worth ratio of as much as 96.5%.

- VA loans: These loans assist you to finance 100% of the house’s buy value, supplying you with a 100% LTV ( no down fee).

- USDA loans: Much like VA loans, the U.S. Division of Agriculture’s (USDA) mortgage program permits a 100% mortgage to worth ratio (or extra) for eligible rural homebuyers.

- Mortgage refinances: For many typical refinances, a mortgage to worth ratio of 80% or decrease is right. This permits householders to keep away from PMI and sometimes qualifies them for one of the best charges.

It’s necessary to notice that whereas these larger mortgage to worth ratios make homeownership extra accessible, they’ll additionally imply larger prices over the lifetime of the mortgage as a result of bigger mortgage quantities and doubtlessly larger rates of interest.

Advantages of a Good LTV

Understanding the advantages of a superb LTV may help you see why lenders place such significance on this metric and why it’s useful to goal for a decrease mortgage to worth ratio when potential.

Simpler Mortgage Approval

Lenders view a decrease mortgage to worth ratio favorably as a result of it signifies much less threat. When you’ve extra fairness within the property relative to the mortgage quantity, lenders are extra assured that you just’ll repay the mortgage and usually tend to approve your software.

Higher Mortgage Phrases

A very good mortgage to worth ratio can typically result in extra favorable mortgage phrases. This will likely embody longer compensation intervals and decrease charges. Lenders are usually extra prepared to supply versatile phrases once they understand the mortgage as much less dangerous. For instance, you may qualify for a 30-year fixed-rate mortgage as an alternative of a shorter-term mortgage, which might make your month-to-month funds extra manageable.

Decrease Curiosity Charges

Lenders have a tendency to provide extra aggressive rates of interest to debtors with decrease mortgage to worth ratios as a result of these loans are thought-about much less dangerous. Even a small discount in your rate of interest can result in substantial financial savings over the lifetime of the mortgage.

Decreased Mortgage Insurance coverage Necessities

For typical loans, a mortgage to worth ratio of 80% or decrease usually means you’ll be able to keep away from paying non-public mortgage insurance coverage. By avoiding this additional expense, you’ll be able to decrease your month-to-month funds and cut back the general price of your mortgage.

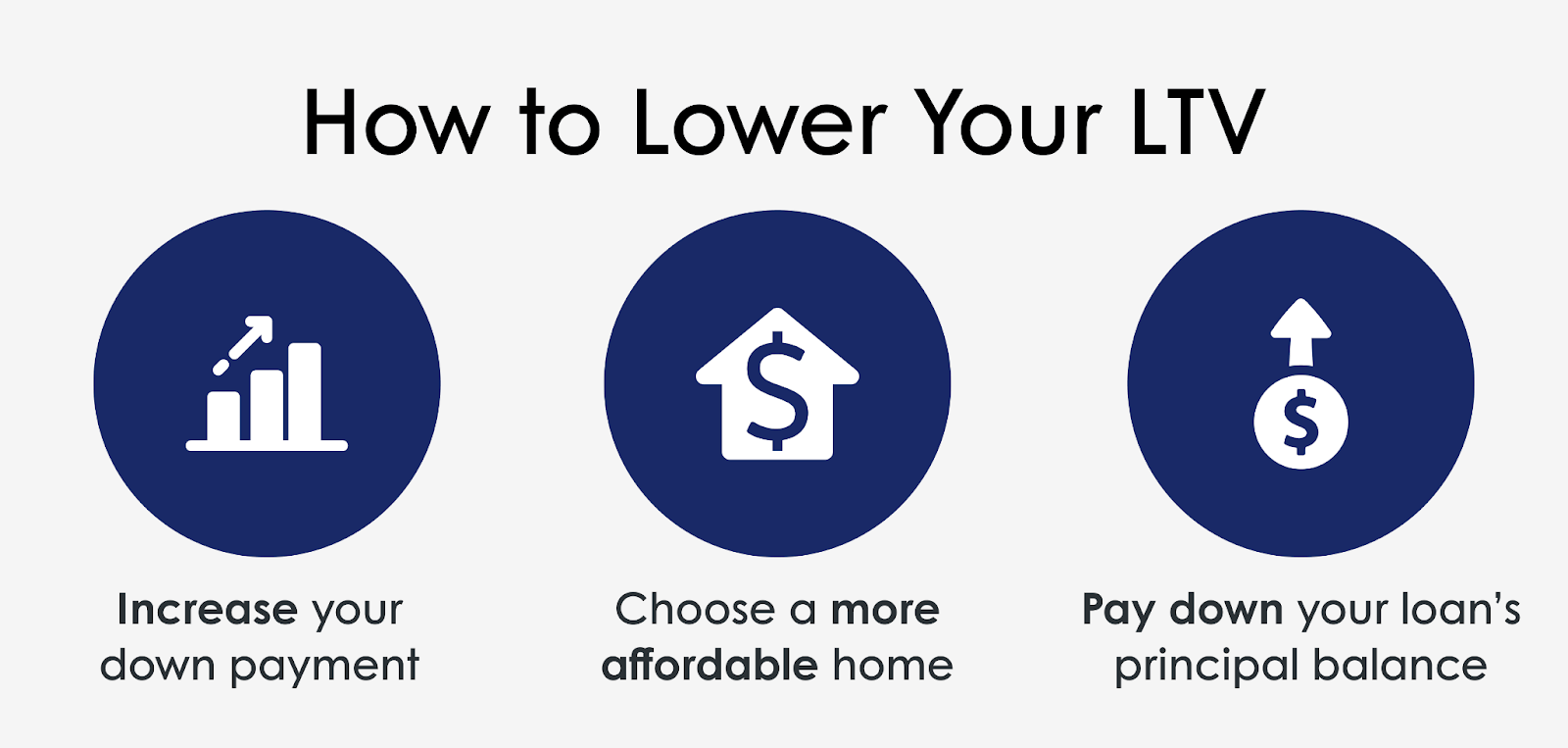

The way to Decrease Your LTV

In case you’re trying to enhance your LTV, there are a number of methods you’ll be able to attempt, similar to:

Enhance Your Down Fee

One of the crucial simple methods to decrease your mortgage to worth ratio is to make a bigger down fee. By placing more cash down upfront, you’re decreasing the quantity it’s essential borrow relative to the property’s worth.

Select a Extra Reasonably priced Residence

One other technique to decrease your mortgage to worth ratio is to think about buying a inexpensive property. By selecting a extra reasonably priced dwelling, you’ll be able to cut back the quantity it’s essential borrow whereas doubtlessly sustaining the identical down fee quantity.

For example, if in case you have $60,000 for a down fee:

- On a $400,000 dwelling, this may be a 15% down fee (85% LTV)

- On a $300,000 dwelling, this may be a 20% down fee (80% LTV)

This method may help you obtain a greater mortgage to worth ratio whereas staying inside your funds.

Pay Down Your Mortgage’s Principal Stability

If you have already got a mortgage, you’ll be able to decrease your mortgage to worth ratio over time by paying down your mortgage’s principal steadiness. As you pay down your principal, your mortgage steadiness decreases whereas your property’s worth doubtlessly will increase, enhancing your mortgage to worth ratio.

Mortgage to Worth: FAQs

Is LTV the one issue lenders take into account?

No, mortgage to worth shouldn’t be the one lending standards thought-about. Whereas LTV is necessary, lenders usually take into account a spread of things to evaluate the general threat of a mortgage.

Typical mortgage lenders typically take into account the next:

- Credit score rating:

- Revenue

- Debt-to-income ratio

- Employment historical past

Exhausting cash lenders, like Supply Capital, typically have totally different priorities. They usually focus extra on:

- The worth of the property serving as collateral

- The potential profitability of the funding (for actual property buyers)

- The borrower’s expertise in actual property investing

- Exit technique for repaying the mortgage

Can my LTV ratio change over time?

Sure, your mortgage to worth ratio can change over time. This may happen as a result of:

- Paying down your mortgage principal, which decreases your mortgage steadiness

- Adjustments in your property’s market worth

- Taking out further loans in opposition to the property

These modifications in your LTV ratio can have an effect on your means to refinance your mortgage. A decrease LTV ratio might qualify you for higher refinancing phrases, whereas a better LTV may restrict your refinancing choices.

How do lenders confirm property worth for LTV calculations?

Lenders usually depend on an expert appraisal to find out the property’s market worth for LTV calculations. A licensed appraiser will assess the property, contemplating current gross sales of comparable properties within the space, the property’s situation and options, and present market developments.

Exhausting Cash Loans with Quick & Simple Approvals

Supply Capital provides same-day approvals and may shut loans in as little as 7-10 days. Whether or not you’re trying to finance residential, industrial, or industrial properties, arduous cash loans can present the capital you want.

At Supply Capital, we provide arduous cash loans in California, Arizona, Colorado, Minnesota, and Texas, providing a streamlined software course of and aggressive phrases for actual property buyers and property house owners in search of various financing options. Apply now!