{kind=link}

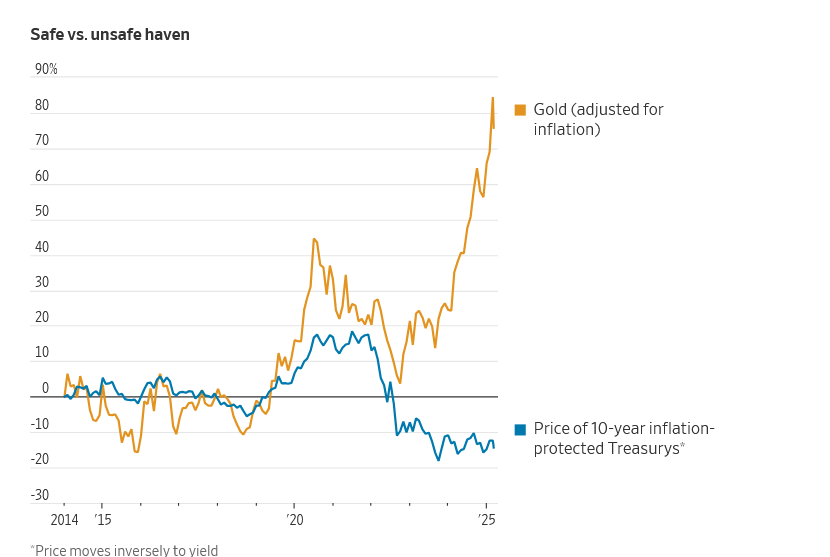

The chart above may be very shocking. When the market is predicting a slowdown or a recession, gold sometimes rises and treasuries additionally rise, sometimes in tandem. The precise reverse is going on now as bond costs are falling and yields are quickly rising within the face of an financial slowdown which is main mortgage charges to prime 7%. Why are mortgage charges not following historic patterns? Will charges fall later this yr? What do you have to do now? What does this imply for the spring actual property market?

Why is the chart so shocking on treasuries?

I used to be floored to see the chart above. The market has been speaking a couple of recession, the inventory market has began to falter and but supposedly the most secure asset, US authorities treasuries have offered off main to large jumps in rates of interest. In each different cycle because the daybreak of treasuries, as quickly as recession speak started, there was a flight to security of US authorities bonds which drove up costs and decreased rates of interest (bear in mind yields and costs transfer in inverse in order costs improve, yields/charges decline and vice versa). What’s driving this big divergence?

There are three drivers of long-term charges

Mortgage charges are internet set by the federal authorities no matter what the media or anybody tries to state. Long run rates of interest are pegged to the ten yr treasury and pushed by the market and future expectations. Beneath are the three essential drivers of rates of interest.

- Inflation Expectations: One of many main drivers of bond costs is pushed by future expectations on inflation. Is the economic system going to develop and are costs going to rise? At the moment inflation is not off course, however the wild card are how tariffs will influence costs and if the tariffs will alter inflation going ahead. Mockingly each measure of inflation is declining, however inflation expectations by customers is rising, so it’s a toss up as to the place we go

- Deficit Spending: Though the DOGE is touting big financial savings, on the finish of the day the deficit continues to develop as the main drivers of the deficit are Medicare/Medicaid, Social Safety, and Protection Spending. None of those large three have been essentially modified to change the deficit path. On prime of the spending, the brand new finances proposal doesn’t seem to maneuver the needle a lot on the deficit. This may finally result in continued provide of US bonds to finance all this debt.

- Market Forces: This refers to fundamental provide and demand. Demand is pushed by traders within the US together with many traders and international locations overseas that park their cash in US treasuries as a result of security and liquidity. The massive demand for treasuries has elevated costs and subsequently stored yields (charges) at historic lows. On the flip facet is provide. The extra provide of treasuries, the decrease the value and the upper the yield (bear in mind they transfer in reverse instructions). The borrowing wants of the US will proceed to develop with deficit spending. The non-partisan congressional workplace (CBO) has confirmed this as nicely with deficits predicted to swell within the coming years

-

- Demand: On the similar time provide is beginning to rise, the demand for treasuries is beginning to wane. Because the delicate touchdown narrative takes maintain there was much less of a flight to “security” property like treasuries. If we do keep away from a recession, then demand for treasuries ought to stay about flat or lower whereas provide will proceed rising.

- New issue Worldwide consumers: Together with demand, there’s a new shift within the treasury market, worldwide consumers like China, Japan, Europe, and so on.. that maintain billions in US debt are rethinking their investing methods and promoting debt and having much less urge for food on the similar time provide is rising, that is resulting in decrease costs and in flip larger yields.

What’s inflicting the drastic swings in mortgage charges?

It has been powerful to maintain monitor of the large swings we’re seeing within the mortgage market. There are two major drivers of the massive worth swings provide/demand pulls and mortgage demand.

- Provide/Demand pulls: 10-year treasury consumers try to determine if demand or provide will finish the tug of battle. Not too long ago treasuries have been overrun with worries about provide which drove up the yields demanded. At the moment provide is one query on everybody’s thoughts as deficits proceed. Search for the provision to proceed to ramp up over the yr which can overtake demand on the longer dated maturities. On the similar time, demand is declining which is a recipe for a lot larger charges and decrease costs.

- Threat Premium: From the chart above on 30year treasuries, the market is frightened about the place long run charges go from right here. The chief concern is provide of treasuries resulting from an enormous deficit that reveals o indicators of easing. As provide will increase finally costs will probably be pushed down and yields will improve. Mortgage consumers subsequently are placing in a danger premium for the longer dated securities as there’s a concern that over the long run charges will settle considerably larger.

Predicted Fed cuts unlikely to materially change actual property in 2025

Sadly the federal reserve is “caught”. Their core mission is worth stability with employment as their second mission. Sadly these two goals are going to class in 25. The federal reserve will prioritize worth stability even with a softening economic system. Moreover, the fed has no management over deficit spending and demand from international consumers. Even when the fed lowers charges, the market possible won’t transfer a lot on long run charges.

Horrible timing for spring market

The surge in rates of interest and teetering of the inventory market couldn’t occur at a worse time for the actual property market. The spring season is often the busiest time in actual property. The financial uncertainty coupled with larger charges goes to place an enormous damper on the actual property market this spring. That is occurring simply as stock is beginning to rise, which can finally result in decrease costs in lots of components of the nation. Though I don’t see an enormous reset in actual property costs, we are going to see substantial softening within the 10-15% vary in lots of markets.

What do you have to do to get the very best charges in 2025?

With charges transferring quickly from daily, what do you have to do? First, full disclosure, I’m not giving monetary recommendation so speak along with your financial institution or mortgage dealer if in case you have questions. Based mostly available on the market there could possibly be some alternatives for decrease charges:

- Have a look at a variable price product: I don’t foresee charges going a lot larger than they’re as we speak so it is likely to be smart to take a look at an adjustable price product to get a decrease price and purchase you time for charges to reset. I’d take a look at 3/1 or 5/1 choices as this could present ample time to see the place the market heads. Notice there’s a danger that charges might see a shock and head even larger so watch out in your timing of a variable price product. Additionally because the spreads tighten between quick and long run charges or probably invert, it would really be cheaper for a hard and fast price. Lengthy and quick, there could possibly be restricted alternatives, but in addition some danger and it’s a must to weigh the profit on the time you lock.

- Be versatile on if you lock in your price: I’d be hesitant to lock in a price too early because the market is transferring shortly. It’s essential be versatile if you lock to reap the benefits of large dips in charges. There must be some alternatives in 2025 as the info is everywhere and may transfer the markets shortly. Now we have seen this within the final couple weeks with half some extent swing inside a couple of days. Be able to lock as quickly as you see a window because the alternatives are going to be very quick.

Abstract:

Don’t purchase the hype that mortgage charges are going to quickly fall as longer-term treasuries are portray a a lot more durable image for mortgage charges. I’ve mentioned for years that deficit spending goes to drive charges larger and we’re seeing that play out. What I didn’t think about was on the similar time demand would pull again resulting from lack of confidence within the US by international consumers of treasuries resulting in even larger charges. Don’t count on the federal reserve to journey in and save the day. These two objects are going to nullify something the federal reserve can do.

Till the US tackles its debt disaster and instills world confidence long run charges together with mortgage charges are going to remain lofty. This will probably be an enormous drawback if the US does enter right into a recession. There will probably be restricted choices to assist the economic system shortly get well which might result in a stagflation state of affairs that we haven’t seen in a long time. Though this isn’t my baseline, it’s undoubtedly a risk because the chart above ought to make you nervous about the place we head.

On a optimistic word, the market appears to be pricing in fairly a little bit of draw back danger so hopefully there will probably be an upside shock with the economic system. We’ll get to see later this yr the way it all works out.

Extra Studying/Sources:

We’re a Personal/ Arduous Cash Lender funding in money!

Glen Weinberg, personally writes all these blogs primarily based on my actual property expertise. I’m not an armchair reporter/author. We’re an precise personal lender, lending our personal cash. We service our personal loans and personal industrial and residential actual property all through the nation.

My day job is and continues to be personal actual property lending/ laborious cash lending which permits me to have a novel perspective available on the market. I don’t settle for any paid sponsorships or advertisements on my weblog to make sure correct info. I’ve been scripting this for nearly 20 years and have over 30k subscribers. Please like and share my blogs on linkedin, twitter, fb, and different social media and ahead to your folks . I’d vastly admire it.

Fairview is a laborious cash lender specializing in personal cash loans / non-bank actual property loans in Georgia, Colorado, and Florida. We’re acknowledged within the trade because the chief in laborious cash lending/ Personal Lending with no upfront charges or some other video games. We fund our personal loans and supply sincere solutions shortly. Study extra about Arduous Cash Lending by way of our free Arduous Cash Information. To get began on a mortgage all we’d like is our easy one web page utility (no upfront charges or different video games).

Written by Glen Weinberg, COO/ VP Fairview Business Lending. Glen has been printed as an professional in laborious cash lending, actual property valuation, financing, and varied different actual property matters in Bloomberg, Businessweek ,the Colorado Actual Property Journal, Nationwide Affiliation of Realtors Journal, The Actual Deal actual property information, the CO Biz Journal, The Denver Submit, The Scotsman mortgage dealer information, Mortgage Skilled America and varied different nationwide publications.

Tags: Arduous Cash Lender, Personal lender, Denver laborious cash, Georgia laborious cash, Colorado laborious cash, Atlanta laborious cash, Florida laborious cash, Colorado personal lender, Georgia personal lender, Personal actual property loans, Arduous cash loans, Personal actual property mortgage, Arduous cash mortgage lender, residential laborious cash loans, industrial laborious cash loans, personal mortgage lender, personal actual property lender